- SS06 Financial Reportingand Analysis (1)

- R19 Introduction to Financial Statement Analysis

- a describe the roles of financial reporting and financial statement analysis;

- b describe the roles of the statement of financial position, statement of comprehensive income, statement of changes in equity, and statement of cash flows in evaluating a company’s performance and financial position;

- c describe the importance of financial statement notes and supplementary information—including disclosures of accounting policies, methods, and estimates—and management’s commentary;

- d describe the objective of audits of financial statements, the types of audit reports, and the importance of effective internal controls;

- e identify and describe information sources that analysts use in financial statement analysis besides annual financial statements and supplementary information;

- f describe the steps in the financial statement analysis framework.

- R20 Financial Reporting Standards

- a describe the objective of financial reporting and the importance of financial reporting standards in security analysis and valuation;

- b describe the roles of financial reporting standard-setting bodies and regulatory authorities in establishing and enforcing reporting standards;

- c describe the International Accounting Standards Board’s conceptual framework, including qualitative characteristics of financial reports, constraints on financial reports, and required reporting elements;

- d describe general requirements for financial statements under International Financial Reporting Standards (IFRS);

- e describe implications for financial analysis of alternative financial reporting systems and the importance of monitoring developments in financial reporting standards.

- R19 Introduction to Financial Statement Analysis

- SS07 Financial Reportingand Analysis (2)

- R21 Understanding Income Statements

- a describe the components of the income statement and alternative presentation formats of that statement;

- b Describe general principles of revenue recognition and accounting standards for revenue recognition;

- c calculate revenue given information that might influence the choice of revenue recognition method;

- d describe general principles of expense recognition, specific expense recognition applications, and implications of expense recognition choices for financial analysis;

- e describe the financial reporting treatment and analysis of non-recurring items (including discontinued operations, unusual or infrequent items) and changes in accounting policies;

- f distinguish between the operating and non-operating components of the income statement;

- g describe how earnings per share is calculated and calculate and interpret a company’s earnings per share (both basic and diluted earnings per share) for both simple and complex capital structures;

- h distinguish between dilutive and antidilutive securities and describe the implications of each for the earnings per share calculation;

- i convert income statements to common-size income statements;

- j evaluate a company’s financial performance using common-size income statements and financial ratios based on the income statement;

- k describe, calculate, and interpret comprehensive income;

- l describe other comprehensive income and identify major types of items included in it.

- R22 Understanding Balance Sheets

- a describe the elements of the balance sheet: assets, liabilities, and equity;

- b describe uses and limitations of the balance sheet in financial analysis;

- c describe alternative formats of balance sheet presentation;

- d distinguish between current and non-current assets and current and noncurrent liabilities;

- e describe different types of assets and liabilities and the measurement bases of each;

- f describe the components of shareholders’ equity;**

- g convert balance sheets to common-size balance sheets and interpret commonsize balance sheets

- h calculate and interpret liquidity and solvency ratios.

- R23 Understanding Cash Flow Statements

- a compare cash flows from operating, investing, and financing activities and classify cash flow items as relating to one of those three categories given a description of the items;

- b describe how non-cash investing and financing activities are reported;

- c contrast cash flow statements prepared under International Financial Reporting Standards (IFRS) and US generally accepted accounting principles (US GAAP);

- d distinguish between the direct and indirect methods of presenting cash from operating activities and describe arguments in favor of each method;

- e describe how the cash flow statement is linked to the income statement and the balance sheet;

- f describe the steps in the preparation of direct and indirect cash flow statements, including how cash flows can be computed using income statement and balance sheet data;

- g convert cash flows from the indirect to direct method;

- h analyze and interpret both reported and common-size cash flow statements;

- i calculate and interpret free cash flow to the firm, free cash flow to equity, and performance and coverage cash flow ratios.

- R24 Financial Analysis Techniques

- a describe tools and techniques used in financial analysis, including their uses and limitations;

- b classify, calculate, and interpret activity, liquidity, solvency, profitability, and valuation ratios;

- c describe relationships among ratios and evaluate a company using ratio analysis;

- d demonstrate the application of DuPont analysis of return on equity and calculate and interpret effects of changes in its components;

- e calculate and interpret ratios used in equity analysis and credit analysis;

- f explain the requirements for segment reporting and calculate and interpret segment ratios;

- g describe how ratio analysis and other techniques can be used to model and forecast earnings.

- R21 Understanding Income Statements

- Financial Reportingand Analysis (3)

- R25 Inventories

- a distinguish between costs included in inventories and costs recognised as expenses in the period in which they are incurred;**

- b describe different inventory valuation methods (cost formulas);

- c calculate and compare cost of sales, gross profit, and ending inventory using different inventory valuation methods and using perpetual and periodic inventory systems;

- d calculate and explain how inflation and deflation of inventory costs affect the financial statements and ratios of companies that use different inventory valuation methods;

- e explain LIFO reserve and LIFO liquidation and their effects on financial statements and ratios;

- f convert a company’s reported financial statements from LIFO to FIFO for purposes of comparison;

- g describe the measurement of inventory at the lower of cost and net realisable value;

- h describe implications of valuing inventory at net realisable value for financial statements and ratios;

- i describe the financial statement presentation of and disclosures relating to inventories;

- j explain issues that analysts should consider when examining a company’s inventory disclosures and other sources of information;

- k calculate and compare ratios of companies, including companies that use different inventory methods;

- l analyze and compare the financial statements of companies, including companies that use different inventory methods.

- R26 Long-lived Assets

- a distinguish between costs that are capitalised and costs that are expensed in the period in which they are incurred;

- b compare the financial reporting of the following types of intangible assets: purchased, internally developed, acquired in a business combination;

- c explain and evaluate how capitalising versus expensing costs in the period in which they are incurred affects financial statements and ratios;

- d describe the different depreciation methods for property, plant, and equipment and calculate depreciation expense;

- e describe how the choice of depreciation method and assumptions concerning useful life and residual value affect depreciation expense, financial statements, and ratios;

- f describe the different amortisation methods for intangible assets with finite lives and calculate amortisation expense;

- g describe how the choice of amortisation method and assumptions concerning useful life and residual value affect amortisation expense, financial statements, and ratios;

- h describe the revaluation model;

- i explain the impairment of property, plant, and equipment and intangible assets;

- j explain the derecognition of property, plant, and equipment and intangible assets;

- k explain and evaluate how impairment, revaluation, and derecognition of property, plant, and equipment and intangible assets affect financial statements and ratios;

- l describe the financial statement presentation of and disclosures relating to property, plant, and equipment and intangible assets;

- m analyze and interpret financial statement disclosures regarding property, plant, and equipment and intangible assets;

- n compare the financial reporting of investment property with that of property, plant, and equipment.

- R27 Income Taxes

- a describe the differences between accounting profit and taxable income and define key terms, including deferred tax assets, deferred tax liabilities, valuation allowance, taxes payable, and income tax expense;

- b explain how deferred tax liabilities and assets are created and the factors that determine how a company’s deferred tax liabilities and assets should be treated for the purposes of financial analysis;

- c calculate the tax base of a company’s assets and liabilities;

- d calculate income tax expense, income taxes payable, deferred tax assets, and deferred tax liabilities, and calculate and interpret the adjustment to the financial statements related to a change in the income tax rate;

- e evaluate the effect of tax rate changes on a company’s financial statements and ratios;

- f distinguish between temporary and permanent differences in pre-tax accounting income and taxable income;

- g describe the valuation allowance for deferred tax assets—when it is required and what effect it has on financial statements;

- h explain recognition and measurement of current and deferred tax items;

- i analyze disclosures relating to deferred tax items and the effective tax rate reconciliation and explain how information included in these disclosures affects a company’s financial statements and financial ratios;

- j identify the key provisions of and differences between income tax accounting under International Financial Reporting Standards (IFRS) and US generally accepted accounting principles (GAAP).

- R28 Non-current (Long-term) Liabilities

- a determine the initial recognition, initial measurement and subsequent measurement of bonds;**

- b describe the effective interest method and calculate interest expense, amortisation of bond discounts/premiums, and interest payments;

- c explain the derecognition of debt;

- d describe the role of debt covenants in protecting creditors;

- e describe the financial statement presentation of and disclosures relating to debt;

- f explain motivations for leasing assets instead of purchasing them;

- g explain the financial reporting of leases from a lessee’s perspective;

- h explain the financial reporting of leases from a lessor’s perspective;

- i compare the presentation and disclosure of defined contribution and defined benefit pension plans;**

- j calculate and interpret leverage and coverage ratios.

- R25 Inventories

- SS09 Financial Reportingand Analysis (4)

- R29 Financial Reporting Quality

- a distinguish between financial reporting quality and quality of reported results (including quality of earnings, cash flow, and balance sheet items);

- b describe a spectrum for assessing financial reporting quality;

- c distinguish between conservative and aggressive accounting;

- d describe motivations that might cause management to issue financial reports that are not high quality;

- e describe conditions that are conducive to issuing low-quality, or even fraudulent, financial reports;

- f describe mechanisms that discipline financial reporting quality and the potential limitations of those mechanisms;

- g describe presentation choices, including non-GAAP measures, that could be used to influence an analyst’s opinion;

- h describe accounting methods (choices and estimates) that could be used to manage earnings, cash flow, and balance sheet items;

- i describe accounting warning signs and methods for detecting manipulation of information in financial reports.

- R30 Financial Statement Analysis: Applications

- a evaluate a company’s past financial performance and explain how a company’s strategy is reflected in past financial performance;

- b forecast a company’s future net income and cash flow;

- c describe the role of financial statement analysis in assessing the credit quality of a potential debt investment;

- d describe the use of financial statement analysis in screening for potential equity investments;

- e explain appropriate analyst adjustments to a company’s financial statements to facilitate comparison with another company

- R29 Financial Reporting Quality

SS06 Financial Reportingand Analysis (1)

R19 Introduction to Financial Statement Analysis

a describe the roles of financial reporting and financial statement analysis;

- financial reporting refers to the way companies show financial performance to investors, creditors, and other interested parties by preparing and presenting financial statements

- financial statement analysis: use information in a company’s financial statements, along with other relevant information, to make economic decisions

- ROLE: financial statement analysis is used to evaluate a company’s past performance and current financial position in order to form opinions about the company’s ability to earn profits and generate cash flow in the future

b describe the roles of the statement of financial position, statement of comprehensive income, statement of changes in equity, and statement of cash flows in evaluating a company’s performance and financial position;

- statement of financial position

- balance sheet: report the firm’s financial position at a point in time

assets resource controlled by firm | liabilities amounts owed to lenders & creditors | equity residual interesr(A minus L)

- accounting equatioin: Assets = Liabilities + ower’s Equity

capital structure: the proportions of liabilities and equity used to finance a company

- statement of comprehensive income

- statement of comprehensive income: report all changes in equity except for shareholder transactions

shareholder transaction: issuing stock, repurchasing stock, paying dividends

- income statement: reports on the financial performance of the firm over a period of time.

aka. the statement of operations or the profit and loss statement

- Revenues: inflows from delivering or producing goods, rendering services, or other activities that constitute the entitys ongoing major or central operations

- Expenses: outflows from delivering or producing goods or services that constitute the entity’s ongoing major or central operations.

- Other income gains that may or may NOT arise in the ordinary course of business

- statement of changes in equity

report the amounts and sources of changes in equity investors’ investment in the firm over a period of time

- statement of cash flow

statement of cash flows reports the companys cash receipts and payments.

- Operating Cash Flows the cash effects of transactions that involve the normal business of the firm

- Investing Cash Flows resulting from the acquisition or sale of PPE; a subsidiary or segment; securities; investments in other firms

- Financing Cash Flows resulting from issuance or retirement of the firms debt and equity securities and include dividends paid to stockholders.

c describe the importance of financial statement notes and supplementary information—including disclosures of accounting policies, methods, and estimates—and management’s commentary;

- Footnotes

Financial statement notes(footnotes)** disclosures that provide further details about the info summarized in the financial statements.

Footnotes:**

- Discuss the basis of presentation (eg. the fiscal period covered and the inclusion of consolidated entities)

- Provide info about accounting methods, assumptions, and estimates used by management

- Provide additional info on items (eg.business acquisitions or disposals, legal actions, employee benefit plans, contingencies and commitments, significant customers, sales to related parties, and segments of the firm)

Managements commentary

aka. management’s report, operating and financial review, and Managements Discussion and Analysis(MD&A)

IFRS guidance recommends that management commentary address the nature of the business. managements objectives, the companys past performance, the performance measures used and the companys key relationships, resources, and risks,

Analysts must be aware that some parts of managements commentary may be un__audited.

For publicly held firms in the United States, the SEC requires that MD&A discuss:

trends and identify significant events and uncertainties that affect the firm’s liquidity, capital resources, and results of operations.

Effects of inflation and changing prices if material Impact of off-balance-sheet obligations & contractual obligations

Accounting policies that require significant judgment by management. Forward-looking expenditures and divestitures

- importance

Allow users to improve their assessments of the amount, timing, and uncertainty of the estimates reported in the financial statements.

d describe the objective of audits of financial statements, the types of audit reports, and the importance of effective internal controls;

- audit and its objective

audit: independent review of an entity’s financial statements.

Public accountants conduct audits and examine the financial reports and supporting records.

objective: enable the auditor to provide an opinion on the_ __fairness _and _reliability _of the financial statements

The auditor examines the company’s accounting and internal control systems, confirms assets and liabilities, and generally tries to determine that there are no material errors in the financial statements.

- types of aduit reports

Standard auditors opinion contains three parts and states that

*the auditor has performed an independent review on financial statements are prepared by management

*assure that the financial statements contain no material errors

*符合会计准则;估算原则合理;对会计方法变动(如果有)的意见

Key Audit Matters (international reports)/ Critical Audit Matters (U.S.): 对财报影响较大的会计选择

| unqualified opinion aka. unmodified or clean opinion |

free from material omissions and errors; | |

|---|---|---|

| modified opinion | qualified opinion | there be exceptions from accounting principles with reasonable explanation |

| adverse opinion | not presented fairly or are materially nonconforming with accounting standards | |

| disclaimer of opinion | unable to express an opinion (in the case of scope limitation) |

- internal controls

Internal controls processes by which the company ensures that it presents accurate financial statements.

⬆responsibility of management ⬆its importance

For publicly traded firms in the United States, the auditor must express an opinion on the firms intemal controls. .

The auditor can provide this opinion separately or as the fourth element of th standard opinion

e identify and describe information sources that analysts use in financial statement analysis besides annual financial statements and supplementary information;

- quarterly or semiannual reports

These interim reports typically update the major financial statements and footnotes but are not necessarily audited.

- proxy statements

代理权公告

issued to shareholders when there are matters that require a shareholder vote. good source of information about ↓

election of (qualifications of) board members, compensation, management qualifications, issuance of stock option

- Corporate reports and press releases

written by management and are often viewed as public relations or sales materials.

not all of the material is independently reviewed by outside auditors. Such info can be found on the companys website.

firms often provide earnings guidance before the financial statements are released.

*after an earnings announcement, a conference call may be held, senior management answer (invetors’) questions

- external information

pertinent information on economic conditions and the companys industry and *competitors.

necessary info can be acquired from trade journals, statistical reporting services, and government agencies.

f describe the steps in the financial statement analysis framework.

- Step 1: **State the objective and context.**

*what questions to answer, the form to be presented, resources available, *time needed

- Step 2: **Gather data **

*Acquire the companys financial statements and other relevant data on its industry and the economy.

*Ask questions of the companys management suppliers, and customers, and visit company sites

- Step 3: **Process the data **

*Make any appropriate adjustments to the financial statements. *Calculate ratios.

*Prepare exhibits such as graphs and common-size balance sheets

- Step 4: **Analyze and interpret the data**

*Use the data to answer the questions stated. *Decide conclusions or recommendations

- Step 5:** **Report the conclusions or recommendations.

*Prepare a report and communicate it to its intended audience.

Be sure the report and its dissemination comply with the Code and Standards

- Step 6: Update the analysis.

Repeat these steps periodically change the conclusions or recommendations when necessary.

R20 Financial Reporting Standards

a describe the objective of financial reporting and the importance of financial reporting standards in security analysis and valuation;

- objective

provide info about the firm to current and potential investors and creditors that is useful for making their decisions about investing in or lending to the firm. __(IASB Condeptual Framework for Financial Reporting)

- importance

financial reporting standards are needed to provide consistency by narrowing the range of acceptable financial reports

- Reporting standards ensure that transactions are reported by firms similarly

Provide important inputs for valuation

b describe the roles of financial reporting standard-setting bodies and regulatory authorities in establishing and enforcing reporting standards;

standard-setting bodies

professional organizations of accountants and auditors that establish financial reporting standards

Financial Accounting Standards Board FASB (u.s.)

‘Generally Accepted Accounting Principles’ G**AAP

International Accounting Standards Board _IASB _(inetrnational)

‘International Financial Reporting Stardards’ _IF__RS**_

- regulatory authorities

government agencies that have legal authority to enforce compliance with financial report standards

Securities and Exchanges Commission SEC (U.S.)

Financial Conduct Authority (UK)

International Organization of Securities Commissions IOSCO

c describe the International Accounting Standards Board’s conceptual framework, including qualitative characteristics of financial reports, constraints on financial reports, and required reporting elements;

The IASB framework details the qualitative characteristics of financial statements and specifies the required elements

Qualitative Characteristics | fundamental** characteristics | relevance | 财报使用者做决策、判断需要的信息;

predict value; confirmatory value; materiality | | —- | —- | —- | | | faithful representation | complete, neutral (absence of bias), free from error | | _enhancing _characteristics | comparability | presentation should be consistent among firms and across the periods | | | verifiability | independent observers, using same methods, obtain similar result | | | timelines | info is available to decision makers before the info is stale | | | understandability** | 易读性;useful info should not be omitted just because it is complicated |Required Reporting Elements | Required Reporting Elements | | | —- | —- | | Assets | resources controlled as a result of past transactions that are expected to provide future economic benefits | | Liabilities | obligations as a result of past events that are expected to require an outflow of economic resources | | Equity | the owners’ residual interest in the assets after deducting the liabilities | | Income | an increase in economics benefits, either increasing assets or decreasing liabilities in a way that increases owners’ equity (but not including contributions by owners).

Income include revenues and gains | | Expenses | decreases in economic benefits, either decreasing assets or increasing liabilities in a way that that decreasing owners’ equity (but not including distributions to owners).

Loss are included in expenses |

| Measurement Base | |

|---|---|

| historical cost | the amount orginally paid for the asset |

| amortized cost | historical cost adjusted for depreciation, amortization, depletion, and impairment |

| current cost | the amount the firm would have to pay today for the same asset |

| net realizable value | the estimated selling price of the asset in the normal course of business minus the selling cost |

| present value | the discounted value of the asset’s expected future cash flows |

| fair value | the price at which an asset could be sold, or a liability tranferred, in an orderly transaction between willing parities |

- Constrains and Assumptions

- Constrains

*tradeoff between accounting cost and info richness

*non-quantifiable info is not included (reputation, brand loyalty. capacity for innovatioin, etc)

- Assumption

accrual accounting: financial statements should reflect transactions at the time the actually occur 权责发生制

⬆not necessarily when cash is paid

going concerns: the company will continue to exist for the foreseeable future

d describe general requirements for financial statements under International Financial Reporting Standards (IFRS);

| Required Financial Statements | |

|---|---|

| Balance sheet | statement of financial position |

| Statement of comprehensive income | |

| Cash flow statement | |

| Statement of changes in owners’equity | |

| Explanatory notes | including a summary of accounting policies |

| Features for Preparing Financial Statements | |

| fair presentation | 对公司交易,以及资产、负债、收入、费用等相关事项正确陈述 |

| going concern basis | 持续经营 |

| accrual basis | 权责发生制 |

| consistency | 不同报告期财报呈现方式具有一致性,同时列有过去财报数据用以对比 |

| materiality | Material info 正确表述+无遗漏 (影响财报使用者决策的info) |

| aggregation | aggregation of similar items and separation of disimilar items |

| no offseting | 除特殊规定,资产负债不相抵,收入费用不相抵 |

| reporting frequency | at least annually |

| comparative information | for prior periods should be included unless a specific stanard states otherwise |

| Structure and Content of Financial Statements | |

| classified balance sheet | showing current and noncurrent assets and liabilities |

| minimum information | BS/CF/Income sheet 有对应的minimum info 要求 |

| comparative information | for prior periods should be included unless a specific stanard states otherwise |

e describe implications for financial analysis of alternative financial reporting systems and the importance of monitoring developments in financial reporting standards.

As financial reporting standards continue to evolve, analysts need to monitor how these developments will affect the financial statements they use.

- new instrument & product 的影响

An analyst should be aware of new products and innovations in the financial markets that generate new types of transactions. These might not fall neatly into the existing financial reporting standards.

The analyst can use the financial reporting framework as a guide for evaluating what effect new products or transactions might have on financial statements

- 跟踪最新standards

To keep up to date on the evolving standards, an analyst can monitor professional journals and other sources, such as the IASB and FASB websites. CFA Institute produces position papers on financial reporting issues through the CFA Institute Centre for Financial Market Integrity

- 跟踪公司财报标准的变化

Analysts must monitor company disclosures for significant accounting standards and estimates change

SS07 Financial Reportingand Analysis (2)

R21 Understanding Income Statements

a describe the components of the income statement and alternative presentation formats of that statement;

income statement

aka. statement of operations, the statement of earnings, or the profit and loss statement (P&L)

Under both U.S. GAAP and IFRS, the income statement and a statement of other comprehensive income can be presented separately or presented together as a single statement of comprehensive income

- components | Components | Definition | Note | | —- | —- | —- | | revenues | amounts from the sales of goods and services in the normal course of bunsiness | net revenue: revenue less adjustments for estimated returns and allowances | | expenses | amounts incurred to generate revenue, include *cost of goods sold, *operating expenses, *interest, and *taxes. | | | gain and losses | result in an increase or decrease of economic benefit | may or may nor result from ordinary business activities. |

income statement equation

<br />

- Presentation formats

- income of subsidiary

When a firm has a controlling interest in a subsidiary, the statements of the two firms are consolidated; the earnings of both firms are included on the income statement.

The noncontrolling interest is subtracted from the consolidated total income to get the net income of parent company不属于母公司的利润要在consolidate时被减去

noncontrolling interest the share (proportion) of the subsidiarys income not owned by the parent(controling interest)

aka minority interest /minority owners’interest

formats

single-step: all revenues are grouped together and all expense are grouped together

multi-step: includes gross profit, revenues minus cost of goods sold

gross profit** 毛利

![[D] Financial Reporting and Analysis - 图2](/uploads/projects/jianzhou@enxqsv/62ff9debd2985c685f804cace97761e1.svg)

operating profit 营业利润

![[D] Financial Reporting and Analysis - 图3](/uploads/projects/jianzhou@enxqsv/b15b148ec7282865cb955871dd912c58.svg)

net income/earnings/bottom line 净利润

![[D] Financial Reporting and Analysis - 图4](/uploads/projects/jianzhou@enxqsv/ab16bff3653d14af8f3aa5cb8dbabdcd.svg) **

**

b Describe general principles of revenue recognition and accounting standards for revenue recognition;

accounts receivable(assets): revenue of a sale made on credit

unearned revenue(liability): payments made before goods/services exchanged

- general priciples

central principle: a firm should recognize revenue when it has transferred a good or service to a customer

- accounting satanards

- five-step process for recognizing revenue:

| 1 | Identify the contract(s) with a customer. | contract: an agreement between two or more parties that specifies their obligations and rights |

|---|---|---|

| 2 | Identify the separate or distinct performance obligations in the contract. | performance obligation: a promise to deliver a _distinct _good or service |

| 3 | Determine the transaction price. | transaction price: the amount a firm expects to receive from a customer |

| 4 | Allocate the transaction price to the performance obligations in the contract. | |

| 5 | Recognize revenue when (or as) the entity satisfies a performance obligation |

- long-term contracts

Revenue is recognized based on a firm’s progress toward completing a performance obligation

Progress toward completion can be measured from

input side (e.g., using the percentage of completion costs incurred as of the statement date)

output side (e.g.,engineering milestones or percentage of the total output delivered to date)

Costs to secure the contract and certain other costs must be capitalized (put on the B/S as an asset).

effect: income statement, reported expenses⬇⋙during the contract period, reported profitability⬆

- required disclosures under the converged standards

Contracts with customers by category.

Assets and liabilities related to contracts, including balances and changes.

Outstanding performance obligations and the transaction prices allocated to them.

Management judgments used to determine the amount and timing of revenue recognition, including any changes to those judgments.

c calculate revenue given information that might influence the choice of revenue recognition method;

| EXAMPLE: Revenue recognition |

|---|

| Performance obligation and progress towards completion |

| A contractor agrees to build a warehouse for a price of $10 million and estimates the total costs of construction at $8 million. Although there are several identifiable components of the building (site preparation, foundation, electrical components, roof, etc.), these components are not separate deliverables, and the performance obligation is the completed building. During the first year of construction, the builder incurs $4 million of costs, 50% of the estimated total costs of completion. Based on this expenditure and a belief that the percentage of costs incurred represents an appropriate measure of progress towards completing the performance obligation, the builder recognizes $5 million (50% of the transaction price of $10 million) as revenue for the year. This treatment is consistent with the percentage-of-completion method previously in use, although the new standards do not call it that. *(percentage of costs incurred used to measure of __progress towards completing the performance obligation) |

| Variable consideration—performance bonus |

| Consider this construction contract with the addition of a promised bonus payment of $1 million if the building is completed in three years. At the end of the first year, the contractor has some uncertainty about whether he can complete building by the end of the third year because of environmental concerns. Because revenue should be recognized only when it is highly probable that it will not be reversed, the builder does not consider the possible bonus as part of the transaction price. In this case, Year 1 revenue is still $5 million, calculated just as we did previously. *(revenue should be recognized only when it is highly probable that it will __not be reversed) During the second year of construction, the contractor incurred an additional $2 million in costs and the environmental concerns have been resolved. The contractor has no doubt that the building will be finished in time to receive the bonus payment. The percentage of total costs incurred over the first two years is now ($4 million + $2 million) / $8 million = 75%. The total revenue to be recognized to date, with the bonus payment included in transaction value, is 0.75 × $11 million = $8.25 million. Because $5 million of revenue had been recognized in Year 1, $3.25 million (= $8.25 million – $5 million) of revenue will be recognized in Year 2. *(_updated _percentage×_updated _Tot R-prior year R) |

| Contract revisions |

| Contracts are often changed over the construction period. The issue for revenue recognition is whether to treat a contract modification as an extension of the existing contract or as a new contract. Returning to our example, a contract revision requires installation of refrigeration to provide cold storage in part of the warehouse. In this case, the contract revision should be considered an extension of the existing contract because the goods and services to be provided are not distinct from those already transferred. The contractor agrees to the revisions during the second year of construction and believes they will increase his costs by $2 million, to $10 million. The transaction value is increased by $3 million, to $14 million, including the bonus, which he believes is still the appropriate treatment. As before, the contractor has incurred $6 million in costs through the end of the second year. Now he calculates the percentage of the contract obligations completed to be $6 million / $10 million = 60%. The total revenue to be recognized to date is 60% × $14 million = $8.4 million. He will report $3.4 million (= $8.4 million – $5 million) of revenue for the second year.*(_updated _percentage×_updated _Tot R-prior year R) |

| Acting as an agent |

| Consider a travel agent who arranges a first-class ticket for a customer flying to Singapore. The ticket price is $10,000, made by nonrefundable payment at purchase, and the travel agent receives a $1,000 commission on the sale. Because the travel agent is not responsible for providing the flight and bears no inventory or credit risk, she is acting as an agent. Because she is an agent, rather than a principal, she should report revenue equal to her commission of $1,000, the net amount of the sale. If she were a principal in the transaction, she would report revenue of $10,000, the gross amount of the sale, and an expense of $9,000 for the ticket. |

d describe general principles of expense recognition, specific expense recognition applications, and implications of expense recognition choices for financial analysis;

- genreal priciples of expense recognition

matching principle: expenses to generate revenue are recognized in the same period as the revenue 收支对应原则

period costs** are expensed in the period incurred

⬆ **expenses not directly tied to revenue generation

- specific expense ercognition applicaion

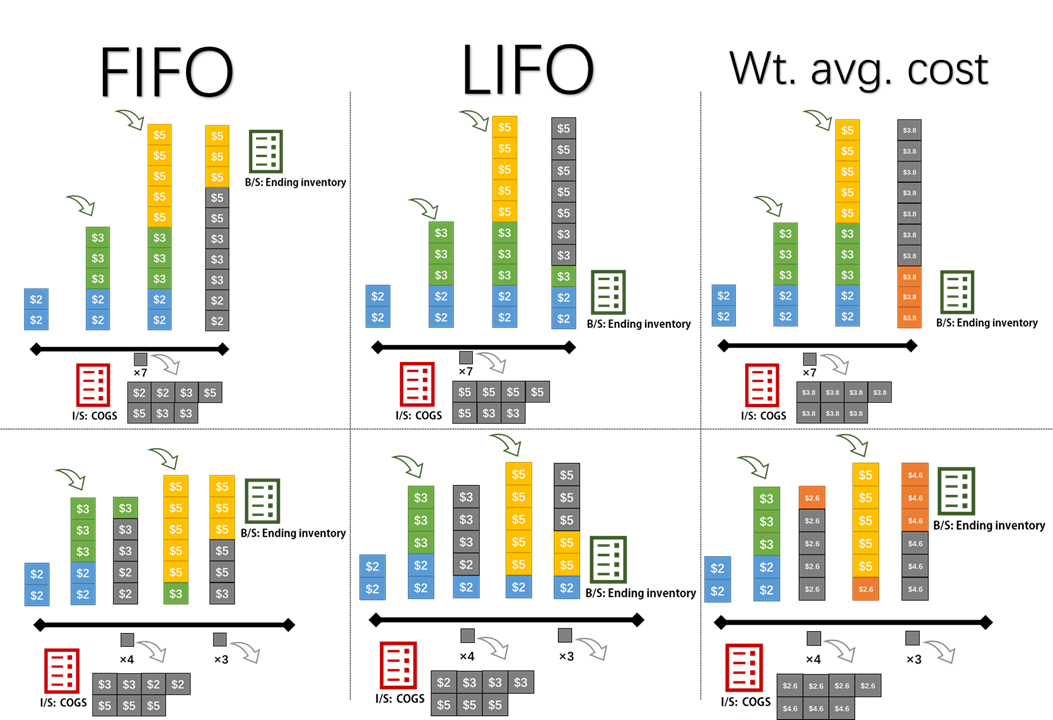

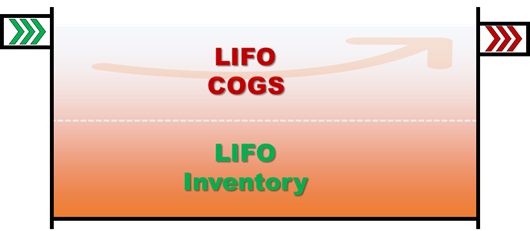

inventory | | U.S. | IFRS | COGS | Ending Inventory | Note | | —- | —- | —- | —- | —- | —- | | specific identification | ✅ | ✅ | | | | | first-in, first-out (FIFO) | ✅ | ✅ | first purchased | most recent purchases | FIFO is appropriate for inventory that has a limited shelf life. | | last-in, first-out (LIFO) | ✅ | ❌ | last purchased | earlist purchase | In an inflationary environment, LIFO results in higher cost of goods sold. Higher cost of goods sold results in lower taxable income and, therefore, lower income taxes.

LIFO is appropriate for inventory that does not deteriorate with age | | weighted average cost | ✅ | ✅ | average cost of all items | average cost of all items | *Average cost results in cost of goods sold and ending inventory values between those of LIFO and FIFO |depreciation

The cost of long-lived assets must also be matched with revenues. Long-lived assets are expected to provide economic benefits beyond one accounting period. The allocation of cost over an asset’s life is known as depreciation (tangible assets), depletion (natural resources), or amortization (intangible assets)

- straight-line depreciation (SL)

![[D] Financial Reporting and Analysis - 图5](/uploads/projects/jianzhou@enxqsv/c82142482b63f95c84489608cf270883.svg)

- accelerated depreciation 加速折旧

speeds up the recognition of depreciation expense in a systematic way

rationale: most assets generate more benefits in the early years of their economic life

declining balance method (DB) 余额递减折旧法

applies a constant rate of depreciation to an asset’s (declining) book value each year.

double-declining balance (DDB) 双倍余额递减法

*depreciation ends once the estimated residual value has been reached.

![[D] Financial Reporting and Analysis - 图6](/uploads/projects/jianzhou@enxqsv/90c5265987c9cdeb8a014835ffcb8792.svg)

对于无残值的资产,余额递减法不能完全折旧,一般在某一时间点转换为直线折旧法

| Assets’ life | straight-line depreciation (SL) | accelerated depreciation |

|---|---|---|

| early years | *lower depreciation expense | *higher depreciation expense |

| *higher net income | *lower net income | |

| later years | *higher depreciation expense | *lower depreciation expense |

| *lower net income | *higher net income | |

| Total depreciation expense SAME |

- amortization

amortization: the allocation of the cost of an intangible asset (such as a franchise agreement) over its useful life.

- straight-line method is most used

- Intangible assets with indefinite lives (e.g., goodwill) are not amortized.

must be tested for impairment at least annuallyexpense recognized on the income statement if impaired

- bed debt & warranty

If a firm sells goods or services on credit or provides a warranty to the customer, the matching principle requires the firm to estimate bad debt expense and/or warranty expense.

i.e. expense is recognized in the period of the sale

- implication for analysis

estimates are involved, possible for firms to delay or _accelerate _the recognition of expenses.

delayed expense recognition increases current net income (more aggressive)

consider the underlying reasons for a change in an expense estimate

compare a firm’s estimates to those of peer firms

find relevsnt info in footnote and _*MD&A_

e describe the financial reporting treatment and analysis of non-recurring items (including discontinued operations, unusual or infrequent items) and changes in accounting policies;

non-recurring items

🅰 discontinued operation

- basic concepts

discontinued operation: *decided to dispose +either * [not yet done , done in the current year after the operation had generated income or losses] 停止经营的项目

measurement date: the date when the company develops a formal plan for disposing of an operation 计划废止

phaseout period: the time between the measurement period and the actual disposal date 计划废止到执废止

- accounting policy

- income/loss is reported *separately in the __I/S, *net of tax, *after income from continuing operations.

- any past I/S presented must be restated, separating income or loss from the discontinued operations.

- on measurement date, the company will accrue any estimated loss during the phaseout period and any estimated loss on the sale of the business.

- any expected gain on the disposal cannot be reported until after the sale is completed. 损失先计,收益后记

analytical implications

- discontinued operations do not affect net income from continuing operations.

- exclude discontinued operations when forecasting future earnings. 做未来收入预测时排除掉

- discontinuing a operation/selling assets may provide info about the future CF of the firm

🅱 unusual or infrequent items

basic concepts

unusual or infrequent items: events are either unusual in nature or infrequent in occurrence

types: *gain/loss of selling assets(not ordinaty); *impairments, *write-offs, *write-downs, *restructuring costs

- analytical implications

- unusual or infrequent items affect net income from continuing operations,

- determine whether unusual or infrequent items should be included when forecasting future earnings.

- whether “unusual or infrequent” losses occur every year or every few years

- changes in acounting policies**

retrospective application: prior-period financial statements MUST be restated

prospective application: prior statements are NOT restated

| change in | accounting policy | accounting estimate | prior-period adjustment |

|---|---|---|---|

| definition / note |

Generally, the result of a change in management’s judgment, usually due to new information | correction of an accounting error made in previous financial statements to meet GAAP/IFRS | |

| requirement | retro**spective ** | pro**spective ** | retro**spective ** |

| anlytical implicaiton |

*accounting estimate changes typically do not affect cash flow. *review changes in accounting estimates to determine their impact on future operating results. |

*prior-period adjustments usually involve errors or new accounting standards *do not typically affect cash flow. *review adjustments carefully because errors may indicate weaknesses in the firm’s internal controls. |

modified retrospective application: does not require restatement of prior-period statements; however, beginning values of affected accounts are adjusted for the cumulative effects of the change

In the recent change to revenue recognition standards, firms were given the option of modified retrospective application**

f distinguish between the operating and non-operating components of the income statement;

Operating and nonoperating transactions are usually reported separately in the I/S.

- nonfinancial firm

nonoperating transactions may result from:

*investment income: investment income & any gains/losses from sale of securities(for inv.) are nonoperating

*financing expenses.: Interest expense is based on the firm’s capital structure, is nonoperating

- financial firm

for a financial firm, investment income and financing expenses are usually considered operating activities.

g describe how earnings per share is calculated and calculate and interpret a company’s earnings per share (both basic and diluted earnings per share) for both simple and complex capital structures;

- basic concepts

earnings per share (EPS) reported only for shares of common stock

simple capital structure: contains no potentially dilutive securities. contains only common stock, nonconvertible debt, and nonconvertible preferred stock Firms with simple capital structures report only basic EPS

complex capital structure contains potentially dilutive securities such as options, warrants, or convertible securities

Firms with complex capital structures must report both basic and diluted EPS

- Baisc EPS

计算公式与影响因素

![[D] Financial Reporting and Analysis - 图7](/uploads/projects/jianzhou@enxqsv/a6bedf2cc6a8010a6aec453f49907e08.svg)

weighted average number of common shares: the number of shares outstanding during the year, weighted by the portion of the year they were outstanding

| stock dividend: distribution of additional shares to each shareholder (proportional to current number of shares)

| stock split: the division of each “old” share into a specific number of “new” (post split) shares

*股票股利和股票分割均不影响股权结构, 但影响计算加权平均流通股数Example

| 计算加权流通股数 —————————- EVENT 1 |

Jan 1 10,000 shares outstanding at the beginning of the year Apirl 1 issues 4,000 new shares July 1**, distribute a 10% stock dividend Sep 1, repurchase 3000 shares** |

||||

|---|---|---|---|---|---|

| start point | Quantity **(adjusted)** | months to Yr end |

weight | sub number | |

| Old shares | Jan 1 | 11,000* =10,000×1.10 | 12 | 1.00 =12/12 | 11,000 =11,000×1.00 |

| Shares issue | April 1 | 4400* =4,000×1.10 | 9 | 0.75 =9/12 | 3,300=4,400×1.00 |

| Shares repurchase | Sep 1 | -3,000** | 4 | 1/3 =4/12 | -1000 =-3,000×1/3 |

| Weighted average shares outstanding | 13,300 | ||||

| *Any shares that were outstanding before the 10% stock dividend must be adjusted for it. **Transactions that occur after the stock dividend do not need to be adjusted. |

|||||

| 计算Basic EPS —————————- EVENT 2 |

net income of $10,000 paid $1,000 cash dividends to preferred shareholders paid $1,750 cash dividends to its common shareholders.* |

||||

| numerator net income – pref. div |

denominator wt. avg. shares of common |

EPS | |||

| $9000=$10,000 – $1,000 | 13,300 | $0.68=$9000/13300 | |||

| *payment of a cash dividend on common shares is NOT considered in the calculation of EPS |

- diluted EPS

![[D] Financial Reporting and Analysis - 图8](/uploads/projects/jianzhou@enxqsv/945ed29ecb2a42cf2853c4ee33d51340.svg)

h distinguish between dilutive and antidilutive securities and describe the implications of each for the earnings per share calculation;

dilutive securities stock options, warrants, convertible debt, or convertible preferred stock that would decrease EPS if exercised or converted to common stock.

antidilutive securities stock options, warrants, convertible debt, or convertible preferred stock that would increase EPS if exercised or converted to common stock.

| numerator | denominator (+dillutive share number) |

||

|---|---|---|---|

| dilutive | convertible preferred stock | +**convertible preferred dividends** | N shares for every $P of par value +**($Value / $P)×N** |

| convertible bonds | -convertible debt interest(1 - t) | N shares for each bonds (par) +**n(bond)×N** |

|

| options / warrants |

do NOT need adjustmet | option price $p*, N options outstanding, average market price over the year $P |

+N(1-$p*/$P) | | antidilutive ** | | do NOT need adjustmet | |

i convert income statements to common-size income statements;

common-size income statement expresses each category of the I/S as a percentage of revenue

effective tax rate: Tax expense is more meaningful when expressed as a percentage of pretax income

⬆In most cases, expressing expenses as a percentage of revenue is appropriate. here’s an exception

j evaluate a company’s financial performance using common-size income statements and financial ratios based on the income statement;

using common-size income statement

using **financial ratios**

gross profit margin: the ratio of gross profit (revenue minus cost of goods sold) to revenue (sales) 毛利率

![[D] Financial Reporting and Analysis - 图9](/uploads/projects/jianzhou@enxqsv/db3e533102374e1eea5feeff7dff60a0.svg)

net profit margin: the ratio of net income to revenue 净利率

![[D] Financial Reporting and Analysis - 图10](/uploads/projects/jianzhou@enxqsv/66fa7e894faa853b25d268b0ba5e8305.svg)

operating profit margin operating profit divided by revenue 营业利润率![[D] Financial Reporting and Analysis - 图11](/uploads/projects/jianzhou@enxqsv/367c93dbb8c4276b3a8e6129c7b8e5c0.svg)

pretax margin pretax accounting profit divided by revenue 税前利润率

![[D] Financial Reporting and Analysis - 图12](/uploads/projects/jianzhou@enxqsv/99510ca35d3b8cb9a5d9a10887f2e7ec.svg)

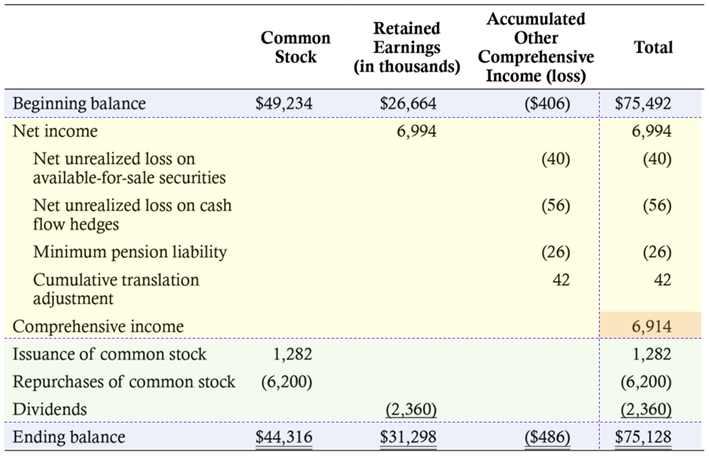

k describe, calculate, and interpret comprehensive income;

- comprehensive income 综合收益

comprehensive income: includes all changes in equity except for owner contributions and distributions

comprehensive **income = net income + other comprehensive income

other comprehensive income (OCI)*:

Foreign currency translation gains and losses. | Adjustments for minimum pension liability.

Unrealized gains and losses from cash flow hedging derivatives. | *Unrealized gains and losses from available-for-sale securities.

|

- comprehensive **income** = net income + other comprehensive income

includes all changes in equity except for owner contributions and distributions | |

| —- | —- |

|

- net income

|

- other comprehensive income (OCI)*

Foreign currency translation gains and losses.

Adjustments for minimum pension liability.

Unrealized gains and losses from cash flow hedging derivatives.

*Unrealized gains and losses from available-for-sale securities. |

retained earnings: an account is used to transferred the net income (less any dividends declared) to stockholders’ equity

unrealized gains and losses: gains/losses in the value of securities that a firm owns and has not yet sold

- 对 investment securities 的处理

| | Categories | Policy for unrealized gains and losses |

| —- | —- | —- |

| U.S.

GAAP | trading securities

debt securities that a firm owns, but intends to sell | reported on the income statement | | | held to maturity

NOT intend to sell prior to maturity | reported at amortized cost on the B/S

(not fair value)

unrealized gains and losses are NOT reported

(neither on I/S or as OCI) | | | available-for-sale securities

not expected to be held to maturity or sold in the near term | reported as other comprehensive income | | IFRS | Securities measured at **fair value through profit and loss** (reoprted on the I/S) | | | | __Securities measured at **amortized cost (NOT reported) | | | | Securities measured at fair value though **other comprehensive income (reoprted as OCI) | |

l describe other comprehensive income and identify major types of items included in it.

R22 Understanding Balance Sheets

a describe the elements of the balance sheet: assets, liabilities, and equity;

balance sheet: reports the firm’s financial position at a point in time

| Assets ————- Resources controlled as a result of past transactions Expected to provide future economic benefits. |

Liabilities ——————- Obligations as a result of past events Expected to require an outflow of economic resources |

|---|---|

| Equity/net assets ————————————- *Owners’ residual interest in the assets after deducting the liabilities |

A financial statement item should be recognized if

future economic benefit (positive/negative) from the item is probable & item’s value or cost can be measured reliably

b describe uses and limitations of the balance sheet in financial analysis;

- uses

- assess a firm’s liquidity, solvency, and ability to make distributions to shareholders

liquidity: the ability to meet short-term obligations

solvency: the ability to meet long-term obligations

- limitations

- problems of value measure

B/S elements should not be interpreted as market value or intrinsic value.

B/S consists of a mixture of values

Value may have changed since the B/S date

- off-balance sheet

There are assets and liabilities that do not appear on the balance sheet but certainly have value

c describe alternative formats of balance sheet presentation;

Both IFRS and U.S. GAAP require firms to separately report their current assets and noncurrent assets and current and noncurrent liabilities.

classified balance sheet: current/noncurrent format, useful in evaluating liquidity

liquidity-based format: present assets and liabilities in the order of liquidity, often used in the banking industry

d distinguish between current and non-current assets and current and noncurrent liabilities;

- background

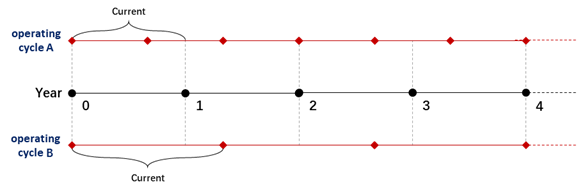

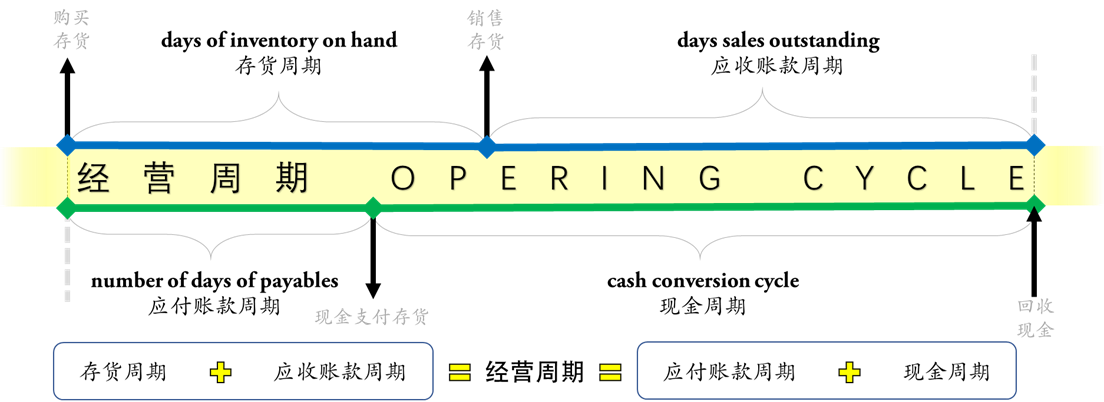

operating cycle: the time it takes to produce or purchase inventory, sell the product, and collect the cash

four subcategories | category | subcategory | explanation | | —- | —- | —- | | assets | current assets | cash/other assets that will likely be converted into cash or used up within max(one year, one operating cycle)

reveal information about the operating activities of the firm | | | noncurrent assets | will not be converted into cash or used up within one year or operating cycle

provide information about the firm’s investing activities (foundation of operation) | | liabilities | current liabilities | obligations that will be satisfied within max(one year, one operating cycle) | | | noncurrent liabilities | |supplementary

working capital: current assets _minus _current liabilities

<br />Not enough working capital may indicate liquidity problems. Too much working capital may indicate an inefficiency

More specifically, a liability that meets any of the following criteria is considered current:

Settlement is expected during the normal operating cycle.

Settlement is expected within one year.

Held primarily for trading purposes.

There is not an unconditional right to defer settlement for more than one year.

e describe different types of assets and liabilities and the measurement bases of each;

- ASSETS

Current Assets🚩

| Cash and cash equivalents | | | —- | —- | | Definition | short-term, highly liquid investments that are readily convertible to cash and near enough to maturity that interest rate risk is insignificant. | | Measrement & Notes | amortized cost or fair value

(either measurement base should result in about the same value.) | | Examples | Treasury bills, commercial paper, and money market funds | | Marketable securities | | | Definition | financial assets that are traded in a public market and whose value can be readily determined | | Measrement & Notes | ③ | | Examples | Treasury bills, notes, bonds, and equity securities | | Accounts receivable/ trade receivables **① | | | Definition | financial assets that represent amounts owed to the firm by customers for goods or services sold on credit | | Measrement & Notes | reported at *net realizable value, (based on estimatedbad debt expense) | | Examples | | | Inventories | | | Definition | goods held for sale to customers or used in manufacture of goods to be sold | | Measrement & Notes | IFRS:

_lower _of cost or net realizable value

*write down when NRV*can be written back up when value recovering

—————————————————————————————————————————————————

U.S. GAAP:

_lower _of cost or market (inventory cost∈[LIFO, retail])

_lower _of cost or net realizable value (inventory cost∉[LIFO, retail])

*write down when market<carrying value

*No write-up is allowed | | Examples | | | Other current assets | | | Definition | include amounts that may not be material if shown separately | | Measrement & Notes | | | Examples | prepaid expenses (operating costs that have been paid in advance ) |

/①/

allowance for doubtful accounts 坏帐准备

contra account 抵消账户used to reduce the value of its controlling account

net realizable value=gross receivables - doubtful account

written off: removed from the balance sheet because they are uncollectible

——————————————————————————————————————————-

/②/

inventory costs

standard costing: assigning predetermined amounts of materials, labor, and overhead to goods produced

retail method: measure inventory at retail prices and then subtract gross profit in order to determine cost

net realizable value = selling price - completion costs - disposal (selling) cost

Market is usually equal to replacement cost;

constraint: net realizable value>**market**>net realizable value - normal profit margin

————————————————————————————————————————————————————————

/③/

financial instruments: contracts that give rise to both a financial asset of one entity and a financial liability or equity instrument of another entity.

Financial instruments can be found on the asset side and the liability side of the balance sheet.

Financial assets include investment securities (stocks and bonds), derivatives, loans, and receivables.

💠U.S. GAAP

| Financial Asset Measurement Bases—U.S. GAAP | ||

|---|---|---|

| TYPE | on B/S | |

| Unlisted equity investments | Historical Cost |

|

| Loans and notes receivable | ||

| Held-to-maturity securities intent to hold until mature |

Amortized Cost |

*original issue price ➖any principal payments, ➕any amortized discount (➖any amortized premium) ➖any impairment losses. =amortized cost |

*subsequent changes in market value are ignored. |

| Trading securities debt,all equity

intent to sell over the near term. | Fair

Value

| unrealized gains and losses (changes in market value before the securities are sold) are recognized in the I/S |

| Available-for-sale securities debtheld to maturity or traded in the near term | | unrealized gains and losses are recognized as OCI as a part of shareholders’ equity |

| Derivatives | | treated the same as trading securities |

| For all financial securities, dividend and interest **income** and realized **gains and losses (actual gains or losses when the securities are sold) are recognized in the I/S** | | |

unrealized gains and losses a.k.a. holding period gains and losses.

fair value a.k.a. mark-to-market accounting

💠**IFRS**

While the three different treatments are essentially the same as those used under U.S. GAAP, there are significant differences in how securities are classified under IFRS and under U.S. GAAP. Similarities and differences are as follows:

| IFRS—Financial Asset Classifications | |

|---|---|

| Debt acquired with the intent to hold them to maturity 持有到期债券 | Measured at amortized cost ≈ held-to-maturity securities (U.S. GAAP) |

| Loans receivable / Notes receivable | |

| Unlisted equity if fair value cannot be determined reliably | |

| Debt acquired with intent to collect interest PMT but sell before maturity | Measured at fair value |

through

OCI

≈ available-for-sale securities (U.S. GAAP) |

| Equity only if this treatment is chosen at time of purchase | |

| Debt acquired with intent to sell in near term | Measured at

fair value

through

profit and loss (I/S)

≈ trading securities (U.S. GAAP) |

| Equity (unless fair value through OCI is chosen at time of purchase) | |

| Derivatives | |

| Any security not assigned to the other two categories | |

| Any security for which this treatment is chosen at time of purchase | |

Noncurrent Assets🚩

| Property, plant, and equipment (PP&E)①** | |

|---|---|

| Definition | tangible assets used in the production of goods and service |

| Measrement & Notes | IFRS: cost model /revaluation model ————————————————————————————————————————————————————- U.S. GAAP: cost model |

| Examples | land and buildings, machinery and equipment, furniture, and natural resources. |

| Investment property | |

| Definition | assets that generate rental income or capital appreciation |

| Measrement & Notes | IFRS: amortized cost (just like PP&E) or fair value ⬆ any change in fair value is recognized in I/S ————————————————————————————————————————————————————- U.S. GAAP: does not have a specific definition |

| Examples | / |

| Deferred tax assets | |

| Definition | created when the amount of taxes payable exceeds the amount of income tax expense recognized in the I/S unused tax losses from prior periods |

| Measrement & Notes | / |

| Examples | / |

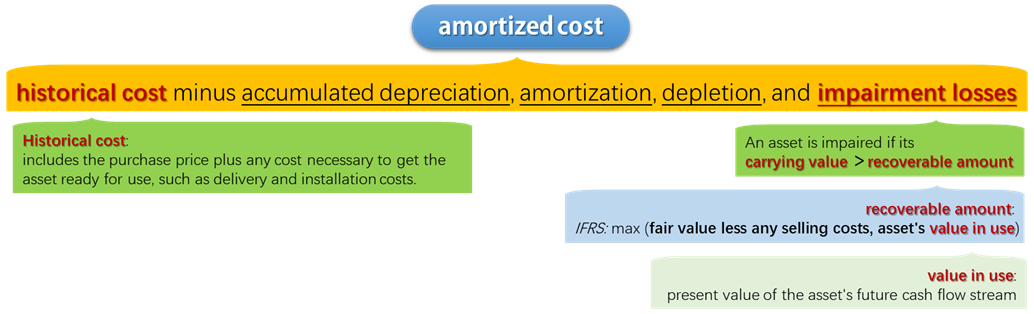

/①/

💠cost model:

Land is not depreciated because it has an indefinite life

PP&E other than land is reported at amortized cost

amortized cost: **historical **cost minus accumulated depreciation, amortization, depletion, and impairment losses).

historical cost: purchase price plus any cost necessary to get the asset ready for use (e.g. delivery and installation costs. )

PP&E must be tested for impairment:

impairment ⬇

An asset is impaired if its carrying value > recoverable amount

If impaired, the asset is written down to its recoverable amount and a loss is recognized in the income statement.

Loss recoveries are allowed under IFRS but not under U.S. GAAP.

*recoverable amount: IFRS max (fair value less any selling costs**, asset’s **value in use)

**value in use**: present value of the asset’s future cash flow stream

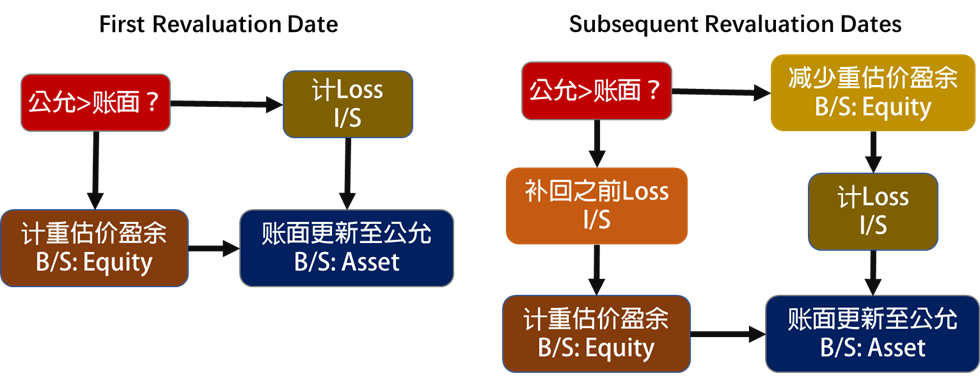

💠revaluation model:

fair value less any accumulated depreciation

changes in fair value are reflected in shareholders’ equity, may be recognized in the I/S in certain circumstances

—————————————————————————————————————————————————————————————-

Intangible Assets🚩

identifiable intangible assets: can be acquired separately or are the result of rights or privileges conveyed to their owner

unidentifiable intangible assets: cannot be acquired separately and may have an unlimited life (e.g. goodwill)

| identifiable intangible assets: purchased | |

|---|---|

| Definition | identifiable intangibles that are purchased |

| Measrement & Notes | IFRS: cost model /revaluation model ⬆ can only be used if an active market for the intangible asset exists ————————————————————————————————————————————————————- U.S. GAAP: cost model |

| Examples | / |

| intangible assets: created internally | |

| Definition | except for certain legal costs, intangible assets that are created internally |

| Measrement & Notes | IFRS: must expense costs in research stage (discovery of new sci or tech knowledge) can capitalize costs in development stage (using research results to plan or design products). ————————————————————————————————————————————————————- U.S. GAAP: expensed as incurred |

| Examples | research and development costs |

| Finite-lived intangible assets | |

| Definition | / |

| Measrement & Notes | amortized over their useful lives and tested for impairment in the same way as PP&E amortization method and useful life estimates are reviewed at least annually |

| Examples | / |

| Infinite-lived Intangible assets | |

| Definition | / |

| Measrement & Notes | not amortized, but are tested for impairment at least annually |

| Examples | goodwill ① |

| all of the following should be expensed as incurred (IFRS & U.S. GAAP) | |

| *| Start-up and training costs. *| Administrative overhead. *| Advertising and promotion costs. *| Relocation and reorganization costs. *Termination costs. |

/①/

Goodwill: the excess of purchase price over the fair value of the identifiable net assets (assets minus liabilities) acquired

Goodwill is ONLY created in a purchase ACQUISITION

*impairment

If impaired, goodwill is reduced and a loss is recognized in the I/S (does not affect cash flow)

As long as goodwill is not impaired, it can remain on the B/S indefinitely.

*accounting goodwill 与 economic goodwill

economic goodwill derives from the expected future performance of the firm

accounting goodwill is the result of past acquisitions.

*implication

⚠ one can allocating more acquisition price to goodwill ➡less depreciation/amortization expense➡higher net income

eliminate goodwill from B/S and goodwill impairment charges from I/S for comparability when computing ratios

evaluate future acquisitions in terms of the price paid relative to the earning power of the acquired assets.

商誉不折旧所以如果恶意将并购额转移至商誉,会产生粉饰效果,降低每年的折旧费用,使net income升高

- LIABILITIES

Current Liabilities🚩

| Accounts payable | | | —- | —- | | Definition | amounts the firm owes to suppliers for goods or services purchased on credit. | | Measrement & Notes | / | | Examples | / | | Notes payable and current portion of long-term debt | | | Definition | obligations in the form of promissory notes owed to creditors and lenders.

notes payable can also be reported as noncurrent liabilities if maturities>one year.

current portion of long-term debt is the principal portion of debt due within one year or operating cycle, whichever is greater. | | Measrement & Notes | / | | Examples | / | | Accrued liabilities a.k.a. accrued expenses | | | Definition | expenses that have been recognized in the I/S but are not yet contractually due | | Measrement & Notes | / | | Examples | interest payable, wages payable, and accrued warranty expense, taxes payable | | Taxes payable | | | Definition | current taxes that have been recognized in the I/S but have not yet been paid | | Measrement & Notes | / | | Examples | / | | Unearned revenue | | | Definition | cash collected in advance of providing goods and services. | | Measrement & Notes | **when received, assets (cash) and liabilities (unearned revenue) increase by the same amount.

*as the product/services are delivered, firm recognizes revenue in the I/S and reduces the liability

——————————————————

*does not require a future outflow of cash like accounts payable

*may be an indication of future growth as the revenue will ultimately be recognized in the I/S. | | Examples | a magazine publisher receives subscription payments in advance of delivery |

Non-Current Liabilities🚩

| Long-term financial liabilities | |

|---|---|

| Definition | / |

| Measrement & Notes | not issued at par→(usually) amortized cost [see in current assets /③/] (in som case) fair value |

| Examples | bank loans, notes payable, bonds payable, and derivatives |

| Deferred tax liabilities | |

| Definition | created when the amount of income tax expense recognized in the I/S > taxes payable |

| Measrement & Notes | / |

| Examples | / |

f describe the components of shareholders’ equity;**

| Concepts | Explanation |

|---|---|

| owners’ equity 所有者权益 | the residual interest in assets that remains after subtracting an entity’s liabilities |

| contributed capital issued capital 实缴资本 |

the amount contributed by equity shareholders |

| par value of common stock | stated or legal value |

| authorized shares | the number of shares that may be sold under the firm’s articles of incorporation |

| issued shares | the number of shares that have actually been sold to shareholders |

| number of outstanding shares | the issued shares less treasury stock |

| preferred stock | stocks that has certain rights and privileges not conferred by common stock |

| noncontrolling interest (minority interest) |

the minority shareholders’ pro-rata share of the net assets (equity) of a subsidiary that is not wholly owned by the parent |

| retained earnings | cumulative undistributed earnings (net income) of the firm since inception |

| treasury stock | stock that has been reacquired but not yet retired |

| accumulated other comprehensive income | all changes in stockholders’ equity except for transactions recognized in the I/S transactions with shareholders, e.g. issuing stock, reacquiring stock, paying dividends |

| statement of changes in stockholders’ equity | summarizes all transactions that increase/decrease the equity accounts for the period |

statement of changes in stockholders’ equity

g convert balance sheets to common-size balance sheets and interpret commonsize balance sheets

common-size balance sheet: expresses each item of the balance sheet as a percentage of total assets.

- The common-size format standardizes the balance sheet by eliminating the effects of size. This allows for comparison over time (time-series analysis) and across firms (cross-sectional analysis).

h calculate and interpret liquidity and solvency ratios.

- liquidity **ratios**

measure the firm’s ability to satisfy its short-term obligations as they come due.

- current ratio

![[D] Financial Reporting and Analysis - 图17](/uploads/projects/jianzhou@enxqsv/0151a535c2276b4b504715038c5e0770.svg)

- quick ratio

![[D] Financial Reporting and Analysis - 图18](/uploads/projects/jianzhou@enxqsv/4f6206e57b0147a30d21fa24ae20c822.svg)

- cash ratio

![[D] Financial Reporting and Analysis - 图19](/uploads/projects/jianzhou@enxqsv/4faab9a6c3e1d96aea42638bf820ff25.svg)

Although all three ratios measure the firm’s ability to pay current liabilities, they should be considered collectively

solvency ratios

measure the firm’s ability to satisfy its long-term obligations.

debt is considered to be any interest bearing obligation.

long-term debt-to-equity

total debt-to-equity

debt ratio

financial leverage

<br />financial leverage ratio captures the impact of all obligations, both interest bearing and non-interest bearing. <br />_All four ratios measure solvency but they should be considered collectively_

- limitations of B/S ratio analysis

- Comparisons with peer firms are limited by differences in accounting standards and estimates.

- Lack of homogeneity as many firms operate in different industries.

- Interpretation of ratios requires significant judgment.

- B/S data are only measured at a single point in time.

R23 Understanding Cash Flow Statements

The cash. flow. statement. provides the following:

Info about a company’s cash receipts and cash payments during an accounting period.

Info about a company’s operating, investing, and financing activities.

An understanding of the impact of accrual accounting events on cash flows.a compare cash flows from operating, investing, and financing activities and classify cash flow items as relating to one of those three categories given a description of the items;

cash flow from operating activities (CFO)

inflows and outflows of cash resulting from transactions that affect a firm’s net income

cash flow from investing activities (CFI)

inflows and outflows of cash resulting from the acquisition or disposal of long-term assets and certain investments

cash flow from financing activities (CFF)

the inflows and outflows of cash resulting from transactions affecting a firm’s capital structure

| U.S. GAAP Cash Flow Classifications | |

|---|---|

| Operating Activities | |

| Inflows | Outflows |

| Cash collected from customers Interest and dividends received Sale proceeds from trading securities |

Cash paid to employees and suppliers Cash paid for other expenses Acquisition of trading securities Interest paid on debt or leases Taxes paid |

| Investing Activities | |

| Inflows | Outflows |

| Sale proceeds from fixed assets Sale proceeds from debt and equity investments Principal received from loans made to others |

Acquisition of fixed assets Acquisition of debt and equity investments Loans made to others |

| Financing Activities | |

| Inflows | Outflows |

| Principal amounts of debt issued Proceeds from issuing stock |

Principal paid on debt or leases Payments to reacquire stock Dividends paid to shareholders |

b describe how non-cash investing and financing activities are reported;

- Noncash investing and financing activities are NOT reported in the cash flow statement since they do NOT result in inflows or outflows of cash

- Noncash transactions must be disclosed in either a footnote or supplemental schedule to the cash flow statement

c contrast cash flow statements prepared under International Financial Reporting Standards (IFRS) and US generally accepted accounting principles (US GAAP);

| Activities | U.S. GAAP | IFRS | | —- | :—-: | :—-: | | Interest received and dividends received | CFO | CFO/CFI | | Dividends paid to the company’s shareholders | CFF | CFO/CFF | | interest paid on the company’s debt | CFO | CFO/CFF | | taxes paid (investing or financing transaction) | CFO | CFO | | taxes paid (investing or financing transaction) | CFO | CFI |

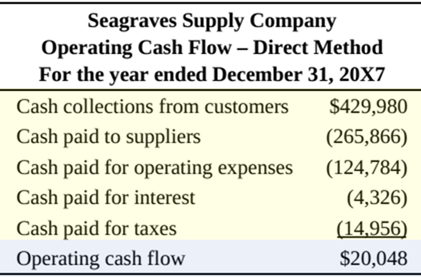

d distinguish between the direct and indirect methods of presenting cash from operating activities and describe arguments in favor of each method;

- direct method

direct method each line item of the accrual-based I/S is converted into cash receipts or cash payments.

the direct method converts an accrual-basis I/S into a cash-basis I/S.

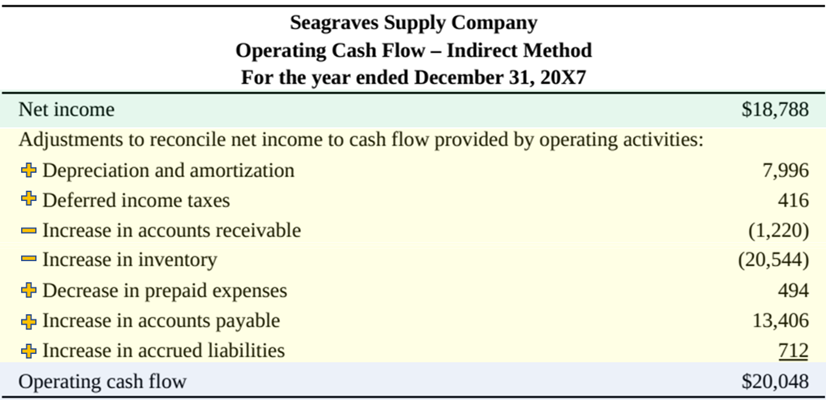

- indirect method

indirect method: convert net income to CFO by making adjustments for transactions that affect net income but are not cash transactions.

These adjustments include eliminating noncash expenses (e.g., depreciation and amortization), nonoperating items (e.g., gains and losses), and changes in B/S accounts resulting from accrual accounting events.

- arguments & disclosure requirements

| | direct method | indirect method |

| —- | —- | —- |

| info richness | 🙂more info

presents the firm’s operating cash receipts and payments | 🙁less info

only presents the net result of these receipts and payments | | | knowledge of past receipts and payments is useful in estimating future operating cash flows | 🙂focus on the difference between net income and CFO | | U.S. GAAP | must also disclose the adjustments necessary

to reconcile net income to CFO (≈用间接法做一次) | | | | payments for interest and taxes can be reported in the cash flow statement or disclosed in the footnotes. | | | IFRS | payments for interest and taxes MUST be disclosed separately in the cash flow statement under either method | |

e describe how the cash flow statement is linked to the income statement and the balance sheet;

adjusting **cash balance** by CF

CF & B/S with a few exceptions

operating activities ↔ current assets & current liabilities.

Investing activities ↔ noncurrent assets

financing activities ↔ noncurrent liabilities & equity.

- B/S items ↔I/S&C/F

Transactions for which the timing of revenue or expense recognition differs from the receipt or payment of cash are reflected in changes in B/S accounts.

![[D] Financial Reporting and Analysis - 图22](/uploads/projects/jianzhou@enxqsv/63b80176b3af63f14710df97782f5cb3.svg) ➡

➡ ![[D] Financial Reporting and Analysis - 图23](/uploads/projects/jianzhou@enxqsv/eb094eff98abd0c352d6f4e4ff0087e7.svg)

f describe the steps in the preparation of direct and indirect cash flow statements, including how cash flows can be computed using income statement and balance sheet data;

* CFO is calculated differently, but the result is the same under both methods.

* The calculation of CFI and CFF is identical under both methods.

* increase in an asset ∽ use of cash (outflow) | decrease in an asset ∽ source of cash (inflow)

* increase in a liability ∽ source of cash (inflow) | decrease in a liability ∽ use of cash (outflow)