- SS14 Fixed Income (1)

- R42 Fixed-Income Securities: Defining Elements

- a describe basic features of a fixed-income security;

- b describe content of a bond indenture;

- c compare affirmative and negative covenants and identify examples of each;

- d describe how legal, regulatory, and tax considerations affect the issuance and trading of fixed-income securities;

- e describe how cash flows of fixed-income securities are structured;

- f describe contingency provisions affecting the timing and/or nature of cash flows of fixed-income securities and identify whether such provisions benefit the borrower or the lender.

- R43 Fixed-Income Markets: Issuance, Trading, and Funding

- a describe classifications of global fixed-income markets;

- b describe the use of interbank offered rates as reference rates in floating-rate debt;

- c describe mechanisms available for issuing bonds in primary markets;

- d describe secondary markets for bonds;

- e describe securities issued by sovereign governments;

- f describe securities issued by non-sovereign governments, quasi-government entities, and supranational agencies;

- g describe types of debt issued by corporations;

- h describe structured financial instruments;

- i describe short-term funding alternatives available to banks;

- j describe repurchase agreements (repos) and the risks associated with them.

- R44 Introduction to Fixed-Income Valuation

- a calculate a bond’s price given a market discount rate;

- b identify the relationships among a bond’s price, coupon rate, maturity, and market discount rate (yield-to-maturity);

- c define spot rates and calculate the price of a bond using spot rates;

- d describe and calculate the flat price, accrued interest, and the full price of a bond;

- e describe matrix pricing;

- f calculate annual yield on a bond for varying compounding periods in a year;

- g calculate and interpret yield measures for fixed-rate bonds and floating-rate notes;

- h calculate and interpret yield measures for money market instruments;

- i define and compare the spot curve, yield curve on coupon bonds, par curve, and forward curve;

- j define forward rates and calculate spot rates from forward rates, forward rates from spot rates, and the price of a bond using forward rates;

- k compare, calculate, and interpret yield spread measures.

- R45 Introduction to Asset-Backed Securities

- a explain benefits of securitization for economies and financial markets;

- b describe securitization, including the parties involved in the process and the roles they play;

- c describe typical structures of securitizations, including credit tranching and time tranching;

- d describe types and characteristics of residential mortgage loans that are typically securitized;

- e describe types and characteristics of residential mortgage-backed securities, including mortgage pass-through securities and collateralized mortgage obligations, and explain the cash flows and risks for each type;

- f define prepayment risk and describe the prepayment risk of mortgage-backed securities;

- g describe characteristics and risks of commercial mortgage-backed securities;

- h describe types and characteristics of non-mortgage asset-backed securities, including the cash flows and risks of each type;

- i describe collateralized debt obligations, including their cash flows and risks.

- R42 Fixed-Income Securities: Defining Elements

- SS15 Fixed Income (2)

- R46 Understanding Fixed-Income Risk and Return

- a calculate and interpret the sources of return from investing in a fixed-rate bond;

- b define, calculate, and interpret Macaulay, modified, and effective durations;

- c explain why effective duration is the most appropriate measure of interest rate risk for bonds with embedded options;

- d define key rate duration and describe the use of key rate durations in measuring the sensitivity of bonds to changes in the shape of the benchmark yield curve;

- e explain how a bond’s maturity, coupon, and yield level affect its interest rate risk;

- f calculate the duration of a portfolio and explain the limitations of portfolio duration;

- g calculate and interpret the money duration of a bond and price value of a basis point (PVBP);

- h calculate and interpret approximate convexity and distinguish between approximate and effective convexity;

- i estimate the percentage price change of a bond for a specified change in yield, given the bond’s approximate duration and convexity;

- j describe how the term structure of yield volatility affects the interest rate risk of a bond;

- k describe the relationships among a bond’s holding period return, its duration, and the investment horizon;

- l explain how changes in credit spread and liquidity affect yield-to-maturity of a bond and how duration and convexity can be used to estimate the price effect of the changes.

- R47 Fundamentals of Credit Analysis

- a describe credit risk and credit-related risks affecting corporate bonds;

- b describe default probability and loss severity as components of credit risk;

- c describe seniority rankings of corporate debt and explain the potential violation of the priority of claims in a bankruptcy proceeding;

- d distinguish between corporate issuer credit ratings and issue credit ratings and describe the rating agency practice of “notching”;

- e explain risks in relying on ratings from credit rating agencies;

- f explain the four Cs (Capacity, Collateral, Covenants, and Character) of traditional credit analysis;

- g calculate and interpret financial ratios used in credit analysis;

- h evaluate the credit quality of a corporate bond issuer and a bond of that issuer, given key financial ratios of the issuer and the industry;

- i describe factors that influence the level and volatility of yield spreads;

- j explain special considerations when evaluating the credit of high yield, sovereign, and non-sovereign government debt issuers and issues.

- R46 Understanding Fixed-Income Risk and Return

SS14 Fixed Income (1)

R42 Fixed-Income Securities: Defining Elements

a describe basic features of a fixed-income security;

- issuer

- Corporations;

- Sovereign national governments

- Non-sovereign governments

- Quasi-government entities

- Supranational entities

- maturity date

maturity date: date on which the principal is to be repaid

term to maturity AKA tenor: the time remaining until maturity

perpetual bonds: no maturity date

money market securities: original maturities of one year or less

capital market securities: original maturities of more than one year

- par value (principal value to be repaid).

par value: the principal amount that will be repaid at maturity

AKA face value, maturity value, redemption value, or principal value of a bond

trading at a discount: 市价<面值 | trading at par: 市价等于面值 | trading at a pr**emium**: 市价>面值

- Coupon rate and frequency.

plain vanilla bond or conventional bond: bond with a fixed coupon rate

zero-coupon bonds or **pure discount bonds:** pay no interest prior to maturity

- Currency in which payments will be made

dual-currency bond:

makes coupon interest payments in one currency and the principal repayment at maturity in another currency

currency option bond:

gives bondholders a choice of which of two currencies they would like to receive their payments in

b describe content of a bond indenture;

trust deed/bond **indenture**: legal contract between the bond issuer (borrower) and bondholders (lenders)

defines the obligations of and restrictions on the borrower and forms the basis for all future transactions (借贷双方)

c compare affirmative and negative covenants and identify examples of each;

- negative covenants: prohibitions on the borrower

restrictions on asset sales

negative pledge of collateral

restrictions on additional borrowings

禁止borrower采取增加违约风险的活动的同时,要避免过于严格的要求导致borrwer错过增长机会 (bad for all parties)

- affirmative covenants: actions the borrower promises to perform

make timely interest and principal payments to bondholders

insure and maintain assets

comply with applicable laws and regulations

d describe how legal, regulatory, and tax considerations affect the issuance and trading of fixed-income securities;

- legal & regulatory

domestic bonds: bonds issued by a firm domiciled in country A and also traded in country A‘s currency

foreign bonds: issued by a firm incorporated in country B, trade on the national bond market of country A in country A‘s currency

panda bonds: bonds issued by foreign firms; trade in China; denominated in yuan

Yankee bonds: firms incorporated outside the USA; trade in the USA; denominated in U.S. dollars

Eurobonds: issued outside the jurisdiction of any one country and denominated in a currency different from the currency of the countries in which they are sold. subject to less regulation than domestic bonds

例:bond issued by a Chinese firm that is denominated in yen and traded in markets outside Japan

global bonds:Eurobonds that trade in the national bond market of a country other than the country that issues the currency the bond is denominated in, and in the Eurobond market?

Eurodollar bonds / euroyen bonds

bearer bonds: ownership is evidenced simply by possessing the bonds

registered bonds: ownership is recorded

- tax considerations

利息收入的税率一般同普通收入税率

市政债券有时具有免税属性

债券在到期前出售,资本利得的税率一般低于普通收入的税率

若长期持有后才出售,资本利得对应的税率可能更低

original issue discount (OID) bonds: bonds sold at significant discounts to par when issued

3. other considerations

- Issuing entities

special purpose entities (SPEs) aka special purpose vehicles (SPVs), bankruptcy remote vehicles

↑ owning specific assets and issuing bonds to provide the funds to purchase the assets

securitized bonds: Bonds issued by SPEs

Sources of repayment | Bond Type | Sources of repayment | | —- | —- | | sovereign bonds | tax receipts | | non-sovereign government entities | general taxes

revenues of a specific project (e.g., an airport)

special taxes or fees dedicated to bond repayment | | corporate bonds | cash generated by the firm’s operations | | securitized bonds | cash flows of the financial assets owned by the SPE | | mortgage-backed security **(MBS)** | principal payments from the mortgages |Collateral

unsecured bonds: a claim to the overall assets and cash flows of the issuer

secured bonds: a claim to specific _assets of a corporation, reduced risk of default

collateral: assets pledged to support a bond issue

equipment trust certificates: debt securities backed by _equipment _eg.railroad cars and oil drilling rigs

collateral trust bonds: backed by financial assets_, eg. stocks and (other) bonds

mortgage-backed security (MBS): underlying assets are a pool of mortgages, and the interest and principal payments from the mortgages are used to pay the interest and principal on the MBS

*covered bonds: segregated underlying assets (cover pool), but remain on the B/S of the issuing corporation (i.e., no SPE is created)

- credit enhancement 信用增级

internal credit enhancement built into the structure of a bond issue

overcollateralization: collateral’s value> debt par value 超额提供抵押

cash reserve fund: cash set aside to make up for credit losses on the underlying assets 现金储备基金

excess spread account: Yield(bonds) <Yield (backing assets) 超额利差

tranches/slices: divide a bond issue into different seniority of claims 优先层级

waterfall structure 瀑布式结构

external credit enhancement provided by a third party

surety bonds: promise to make up any shortfall in the cash available to service the debt 履约保证

bank guarantees: 银行担保 |作用同履约保证

letter of credit: 承诺在公司还债困难时向公司提供借款

e describe how cash flows of fixed-income securities are structured;

principal: the amount borrowed | coupons: interest payments

- payment structure

bullet structure: coupon payments are made over the life of the bond,

principal value is paid with the final interest payment at maturity

balloon payment: the final payment includes a lump sum in addition to the final period’s interest

amortizing loan: periodic payments include both interest and some repayment of principal

fully amortizing: principal is fully paid off when the last periodic payment is made

partially amortizing: a balloon payment at bond maturity

sinking fund provisions: provide for the repayment of principal through a series of payments over the life of the issue

‘偿债基金条款’ 优:本金逐渐收回,降低违约风险;缺:低利率时期面临再投资风险

eg. a 20-year issue with a face amount of $300 million may require that the issuer retire $20 million of the principal every year beginning in the sixth year

- coupon (rate) arrangment

- coupon rate

floating-rate notes (FRN) AKA floaters: periodic interest depends on a current market rate

reference rate: market rate of interest

basis points: 0.01%

cap: 利率顶 | floor: 利率底

inverse floater: coupon rate 与 reference rate 反向变动

- coupon payment

step-up coupon bonds: coupon rate increases over time according to a predetermined schedule 递增票息债券

credit-linked coupon bond: credit rating of issuer falls ⋙coupon rate increases by a certain amount 反之亦然

payment-in-kind (PIK) bond: make the coupon payments by increasing the principal amount of the bonds

↑paying bond interest with more bonds.

deferred coupon bond aka split coupon bond: 债券发行一段时间后才进行coupon payments。递延付息债券

- index-linked

index-linked bond: coupon payments and/or a principal value that is based on a index 票息或本金都可以作为connector

inflation-linked bonds aka linkers: payments are based on the change in an inflation index

principal protected bonds: 即使指数下跌,到期本金偿还不会少于面值的indexed bonds

indexed-annuity bonds: fully amortizing bonds, periodic payments directly adjusted for inflation or deflation

indexed zero-coupon bonds: payment at maturity is adjusted for inflation

interest-indexed bonds: coupon rate is adjusted for inflation while the principal value remains unchanged

capital-indexed bonds: coupon rate remains constant, principal value is increased by the rate of inflation.

↑most common type. eg. U.S. Treasury Inflation Protected Securities (TIPS)

f describe contingency provisions affecting the timing and/or nature of cash flows of fixed-income securities and identify whether such provisions benefit the borrower or the lender.

- basic concepts

contingency provision: an action that may be taken if an event (the contingency) actually occurs

embedded options: contingency provisions in bond indentures 嵌入期权

straight/option-free bonds: bonds that do not have contingency provisions 普通债券(不含全)

- callable bonds 可赎回债券

call option: issuer has the right to redeem all or part of a bond issue at a specific price (call price)

the call price puts an upper limit on the value of the bond in the market

a callable bond must offer a higher yield (sell at a lower price) than an otherwise identical noncallable bond

callable bond 对发行者有利,所以必须提高更高的收益率

call schedule eg.↓

| The bonds can be redeemed by the issuer at 102% (call price)of par after June 1, 2017 (first call date) . The bonds can be redeemed by the issuer at 101% of par after June 1, 2020. The bonds can be redeemed by the issuer at 100% of par after June 1, 2022 (first par call __date). |

|---|

lockout period aka cushion, deferment period 不能行使赎回权的时期,停摆期

call premium: the amount by which the call price is above par 赎回溢价

styles of exercise for callable bonds

American style—the bonds can be called anytime after the first call date. 美式期权

European style—the bonds can only be called on the call date specified.欧式期权

Bermuda style—the bonds can be called on specified dates after the first call date, often on coupon payment dates. 百慕大

*make-whole: 赎回价格不固定,根据所有未得支付的票息的现值总和。净效果:有赎回权,但赎回可能要付出成本

- putable bonds

put option: bondholder have right to sell the bond back to the issuing company at a prespecified price, typically par

putable bond赋予债券人好处,所以收益率会低于无权债券(价格更高)

- convertible bonds

convertible bonds: bondholders have option to exchange the bond for a specific number of shares of common stock.

aka hybrid security 既像股票又像债券:相对于普通股:有利息收入;相对于不含权债券:利率较低,但可能获得更大收益(行权)

conversion price: the price per share at which the bond (at its par value) may be converted to common stock

conversion ratio: [par value of the bond]/[conversion price]![[G] Fixed Income - 图1](/uploads/projects/jianzhou@enxqsv/46d11c693ed024c141d7b51b98175f85.svg)

conversion value: the market value of the shares that would be received upon conversion

许多可转债同时含有可赎回条款,当conversion value显著高于债券面值时,公司可通过行使赎回权强迫债券只有人将债券转换为股票

(因债权人若write the call option 将面临更多损失) ↑

- warrants** **

warrants: 债券持有人有权在特定时间以特定价格购入发行人公司的普通股

warrants通常与straight bond绑定发行,降低发债成本,作为sweetener

- Contingent Convertible Bonds** **

contingent convertible bonds (CoCos) : 若指定事件发生,债券将自动由debt(负债)转换为common stock(权益)

银行发行较多,当银行权益资本下降时,债券自动转换为普通股以维持资本充足率 “应急可转债”

R43 Fixed-Income Markets: Issuance, Trading, and Funding

a describe classifications of global fixed-income markets;

| 1 | Type of issuer | households, nonfinancial corporations, governments, and financial institutions. |

|---|---|---|

| 2 | Credit quality | Standard & Poor’s (S&P), Moody’s, and Fitch; 投资级/非投资级 |

| 3 | Original maturities | money market securities/ capital market securities |

| 4 | Coupon structure | floating-rate or fixed-rate bonds |

| 5 | Currency denomination | majority of bonds issued are denominated in either U.S. dollars or euros |

| 6 | Geography | developed markets / emerging markets |

| 7 | Indexing | index-linked bonds |

| 8 | Tax status | municipal bonds, or munis |

b describe the use of interbank offered rates as reference rates in floating-rate debt;

London Interbank Offered Rate (LIBOR) : LIBOR rates are published daily for several currencies and for maturities of one day (overnight rates) to one year | maturities ∈[1 day, 1year] | eg. 30-day U.S. dollar LIBOR; 90-day Swiss franc LIBOR

interbank money market: the global network utilized by financial institutions to trade currencies between themselves.

structured overnight financing rate (SOFR): based on the actual rates of repurchase (repo) transactions and reported daily by the Federal Reserve

Shanghai Interbank Offered Rate (Shibor) 上海银行间同业拆放利率

c describe mechanisms available for issuing bonds in primary markets;

primary market: sales of newly issued bonds

public offering: newly issued bonds registered with securities regulators

private placement: newly issued bonds sold only to qualified investors

steps of a public offering

Determining funding needs.

Structuring the debt security.

Creating the bond indenture.

Naming a bond trustee (a trust company or bank trust department).

Registering the issue with securities regulators.

Assessing demand and pricing the bonds given market conditions.

Selling the bonds.

underwritten offering or a best efforts offering

For larger issues, the lead underwriter heads a syndicate of investment banks who collectively establish the pricing of the issue and are responsible for selling the bonds to dealers, who in turn sell them to investors.

grey market

primary dealers: participate in purchases and sales of bonds with the central bank 一级交易商

*shelf registration: Bonds can then be issued over time when the issuer needs to raise funds 暂搁注册

d describe secondary markets for bonds;

secondary markets: the trading of previously issued bonds

e describe securities issued by sovereign governments;

sovereign governments: national gov. or their treasuries issue bonds backed by the taxing power of the government.

本币发行的政府债券信用更高,因为实在不行可以启用印钞机。

on-the-run bonds/ benchmark bonds: most recently issued government securities of a particular maturity

f describe securities issued by non-sovereign governments, quasi-government entities, and supranational agencies;

non-sovereign government bonds: issued by states, provinces, counties, and sometimes by entities created to fund and provide services such as for the construction of hospitals, airports, and other municipal services. 地方政府债券

agency or quasi-government bonds: issued by entities created by national governments for specific purposes such as financing small businesses or providing mortgage financing 准政府组织债券

government-sponsored enterprises (GSEs)

supranational bonds: issued by supranational agencies, also known as multilateral agencies 超国家债券

g describe types of debt issued by corporations;

- Bank Debt** **

bilateral loan: loan involves only one bank 双边贷款(仅包含一家银行)

syndicated loan: a loan is funded by several banks

- Commercial Paper

commercial paper: short-term, unsecured debt instrument, issued by larger creditworthy corporations

bridge financing: debt that is temporary until permanent financing can be secured 过渡融资

rolled over 展期 | rollover risk 展期风险

backup lines of credit 备用信用额度

add-on yield: the percentage interest paid at maturity in addition to the par value of the commercial paper 分母为面值

- Corporate Bonds

serial bond issue: bonds are issued with several maturity dates so that a portion of the issue is redeemed periodically

term maturity structure: all the bonds maturing on the same date

medium-term notes (MTNs): issued in various maturities, ranging from nine months to periods as long as 100 years. Issuers provide maturity ranges for MTNs they wish to sell and provide yield quotes for those ranges. 中期票据

h describe structured financial instruments;

structured financial instruments: securities designed to change the risk profile of an underlying debt security, often by combining a debt security with a derivative. 结构化金融工具,用于改变债券的风险属性(常用方式:结合衍生产品)

- Yield enhancement instruments** **

credit-linked note (CLN): regular coupon payments, but its redemption value depends on whether a specific credit event occur. Purchasing a CLN can be viewed as buying a note and simultaneously selling a credit default swap (CDS)

- Capital protected instruments** **

capital protected instrument: offers a guarantee of a minimum value at maturity, with some potential upside gain

Such a security could be created by combining a zero-coupon bond+option.

guarantee certificate: guaranteed payoff is equal to the initial cost of the structured security

- Participation instruments** **

participation instrument: payments that are based on the value of an underlying instrument

可用于规避投资限制 often a reference interest rate or equity index. ↑

eg. floating-rate note: coupon payments are based on the value of a short-term interest rate

- Leveraged instruments** **

inverse floater

- leveraged inverse floater eg. C = 6% - (1.2 × 90-day LIBOR)

- deleveraged inverse floater eg. C = 7% – (0.5 ×180-day LIBOR)

In either case, a minimum or floor rate for the coupon rate, often 0%, is specified for the inverse floater.

i describe short-term funding alternatives available to banks;

- retail deposits aka customer deposits: transactions services, immediate availability *typically no interest 零售存款

- money market mutual funds and savings accounts: less liquidity, less transactions services, pay periodic interest

- certificates of deposit (CDs) mature on specific dates, offered in a range of short-term maturities 定期存单

negotiable certificates of deposit can be sold 可转让大额定期存单

- interbank funds: funds that are loaned by one bank to another

central bank funds market where a bank can borrow excess reserves from other banks

central bank funds rates: rates for transactions in central bank funds market

j describe repurchase agreements (repos) and the risks associated with them.

- basic concepts

repurchase (repo) agreement: one party sells a security to a counterparty with a commitment to buy it back at a later date at a specified (higher) price 回购协议

repo price 回购价格 | repo rate 回购利率 (annualized)

eg. a firm that enters into a repo agreement to sell a 4%, 12-year bond with a par value of $1 million and a market value of $970,000 for $940,000 and to repurchase it 90 days later for $947,050

asset 属性:4%, 12-year bond with a par value of $1 million, market value: $970,000

selling price (amount loaned): $940,000

repo price: $947,050; repo date: 90 days later; repo margin: 940000**/970000-1= –3.1%

注意这里的repo margin是指融资额与市价的比较

repo margin aka haircut: the percentage difference between the market value and the amount loaned 存在haircut,本质上变得更像抵押贷款

reverse repo agreement** 逆回购协议

- risks

| Items | Influence Factor |

| —- | —- |

| repo rate

| Higher, the longer the repo term.

Lower, the higher the credit quality** of the collateral security.

Lower when the collateral **security is delivered to the lender.

Higher when the interest rates for alternative sources of funds are higher. | | repo margin | Higher, the longer the repo term.

Lower, the higher the credit quality of the collateral security.

Lower, the higher the credit quality of the borrower.

Lower when the collateral security is in high demand or low supply. |

R44 Introduction to Fixed-Income Valuation

a calculate a bond’s price given a market discount rate;

yield-to-maturity (YTM) aka redemption yield: market discount rate appropriate for discounting a bond’s cash flow

bond with **annual **coupon payments

![[G] Fixed Income - 图2](/uploads/projects/jianzhou@enxqsv/e31c23373aea1fac823bc74f6b4fada7.svg)

bond with **semiannual **coupon payments

![[G] Fixed Income - 图3](/uploads/projects/jianzhou@enxqsv/14940b0747369bbdab082ae9baab47be.svg)

Using Calculator

[N] number of period | [PMT] the periodic coupon payment | [FV] the par value or selling price at the end of an holding period

[I/Y] periodic discount rate | [PV] PV of the bond’s cash flows | [CPT] ‘CPT 1 unknown with 4 known’

- key characteristics

bond yields ⬇, market value (PV) ⬆;

bond yields ⬆, market value (PV) ⬇.,

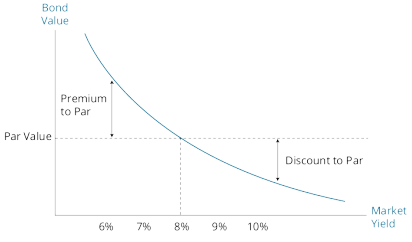

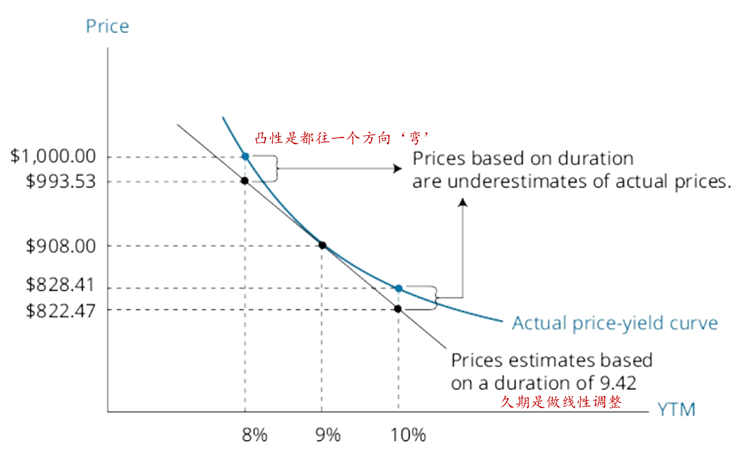

b identify the relationships among a bond’s price, coupon rate, maturity, and market discount rate (yield-to-maturity);

- General Relationship

| | influence on bond’s price |

| —- | —- |

| coupon rate | coupon rate>YTM, price>par value, 溢价premium

coupon rate

d(price)/d(YTM)是递减函数,YTM水平越高,相同YTM变化带来的债券价格下跌越少 |

eg. Market Yield vs. Bond Value for an 8% Coupon Bond↓

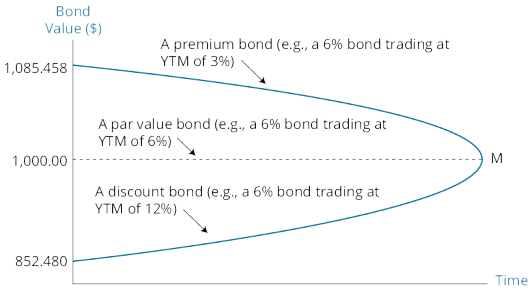

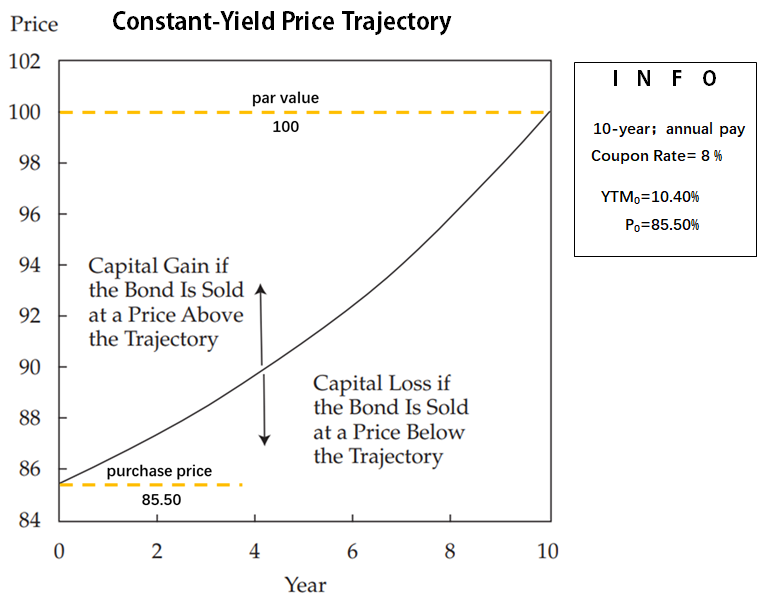

- Relationship Between Price and Maturity** **

在持有期内出售债券,其价格可能会明显高于/低于债券的面值

债券价格会在逐渐到期的过程中回归到其面值

constant-yield price trajectory: convergence to par value at maturity

折价、平价、溢价债券价格逐渐回归值面值的过程

c define spot rates and calculate the price of a bond using spot rates;

- spot rates and no-arbitrage price of bond

spot rates aka zero-coupon rates, zero rates: market discount rates for a single payment in the future

the discount rates for zero-coupon bonds are spot rates

no-arbitrage price of a bond: 用spot rates计算得出的债券价格

![[G] Fixed Income - 图6](/uploads/projects/jianzhou@enxqsv/fbd274975d910d8b8cd7505bc8ed4741.svg)

S**i** spot rates for maturity i

- application

根据[S1,S2,…,SN],[PMT],[par value(FV)],计算[PV]

根据PV和par value的相对大小,判断折价/平价/溢价发行,以及coupon rate 和YTM的相对大小

here,YTM隐含在通过spot rate计算出的债券价格中,而非直接从市场上获得

根据[PV], [PMT], [I/Y], [N], 计算[*YTM]

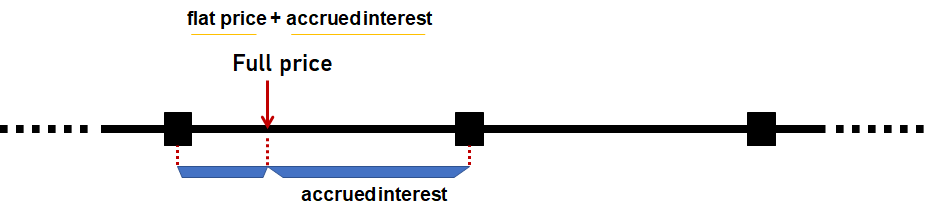

d describe and calculate the flat price, accrued interest, and the full price of a bond;

利用YTM计算出的PV对应时间点是债券发行日,或某一coupon payment day

- full price

aka. dirty price![[G] Fixed Income - 图7](/uploads/projects/jianzhou@enxqsv/ff0febf5131a1da33006c4e9fcbc925f.svg)

t: 距上次付息日的天数 | T: 一个计息期的总天数

accrued interest

genral fomula

![[G] Fixed Income - 图8](/uploads/projects/jianzhou@enxqsv/9b9e66861a781a95272735cc23eea07f.svg)

t = number of days from the last coupon payment to the settlement date

T = number of days in the coupon period

t/T = fraction of the coupon period that has gone by since the last payment

PMT = coupon payment per period30/360 method 公司债券常用

actual/actual method 政府债券常用

flat price

aka. clean price or quoted price

![[G] Fixed Income - 图9](/uploads/projects/jianzhou@enxqsv/730241cfc373bc56878a4c5208cec4cd.svg)

Note that the flat price is NOT the present value of the bond on its last coupon payment date

flat price不对应任何一点的PV?

e describe matrix pricing;

matrix pricing: use the YTMs of traded bonds that have credit quality very close to that of a nontraded or infrequently traded bond and are similar in maturity _and _coupon, to estimate the required YTM

- linear interpolation

s1 选择相近信用等级,相同票息结构的债券

s2 求每一maturity对应的YTM的均值

s3 线性插值计算目标债券的YTM:

![[G] Fixed Income - 图11](/uploads/projects/jianzhou@enxqsv/1871608fb6bca16d14cebc2349172e36.svg)

s4 根据YTMx计算目标债券的market price

- pricing with spreads | maturity | 5-year | 6-year | 7-year | | —- | —- | —- | —- | | Bond A | YTMA5 | YTMA6 | YTMA7 | | Bond B | YTMB5 | YTM**B6=YTMA6+spread 6 | YTMB7 | | spread i | YTMB5 -YTMA5 | spread 6**= average (spread 5, spread 7,…) | YTMB7 -YTMA7 |

f calculate annual yield on a bond for varying compounding periods in a year;

By convention, the YTM on a semiannual coupon bond is expressed as two times the semiannual discount rate.

periodicity of a bond: the number of bond coupon payments per year

It may be necessary to adjust the quoted yield on a bond to make it comparable with the yield on a bond with a different periodicity

将年内计息次数调整到相同的水平后,债券价格才具有可比性。(例如均调整为连续复利)

计算政府债券和公司债券的spread时,一般将公司债券的天数计算惯例由(30/360)调整为(actual/actual)

- annual yield

annual (effective) yield:

![[G] Fixed Income - 图12](/uploads/projects/jianzhou@enxqsv/0373b20d3c18032817e1763dfb0d7699.svg)

street convention: Bond yields calculated using the stated coupon payment dates

true yield: yield calculated using these actual coupon payment dates 考虑假期导致的付息延迟,true yield会稍小

- 其他yield

current yield aka income yield, running yield: 当期收益率

![[G] Fixed Income - 图13](/uploads/projects/jianzhou@enxqsv/e961966302c047e5b75137b53cbeb952.svg)

simple yield: takes a discount or premium into account by assuming that any discount or premium declines evenly over the remaining years to maturity [公式有问题]

![[G] Fixed Income - 图14](/uploads/projects/jianzhou@enxqsv/e6278b00bda7af9cb151b174309c39e2.svg)

yield-to-call: yield for each possible call date and price

yield-to-worst: the lowest of yield to-maturity and the various yields-to-call

option-adjusted yield: calculated by adding(?) the value of the call option to the bond’s current flat price

g calculate and interpret yield measures for fixed-rate bonds and floating-rate notes;

paid in arrears: coupon rate for the next period is set using the current reference rate for the reset period, and the payment at the end of the period is based on this rate

quoted margin: margin used to calculate the bond coupon payments

required margin** aka discount **margin: margin required to return the FRN to its par value

| FRN’s credit quality | margin的相对大小 | when the next coupon payment |

|---|---|---|

| unchanged | quoted margin =required margin | FRN returns to its par value |

| decreased | quoted margin<required margin | FRN will sell at a discount to its par value |

| improved | quoted margin>required margin | FRN will sell at a premium to its par value. |

A somewhat simplified way of calculating the value of an FRN on a reset date is to discount these future cash flows at the reference rate plus the required (discount) margin. More complex models produce better estimates of value

h calculate and interpret yield measures for money market instruments;

U.S. Treasury bills, quoted as annualized discounts from face value based on a 360-day year

LIBOR and bank CD rates, quoted as add-on yields

add-on yields:

![[G] Fixed Income - 图15](/uploads/projects/jianzhou@enxqsv/978f8a43edac934a7ec2623742b8190c.svg)

注:声明add-on yields时,必需标明day base,因为没有把期限标准化

bond equivalent yield: add-on yield based on a 365**-day year

将bond equivalent yield 转化为semiannual basis

| input | t: security maturity BEY: bond equivalent yield |

|---|---|

| 1 将BEY转化为add-on yield | |

| 2 将add-on yield转换为EAR | |

| 3 将EAR转换为semiannual | |

| 4 转换成YTM形式 |

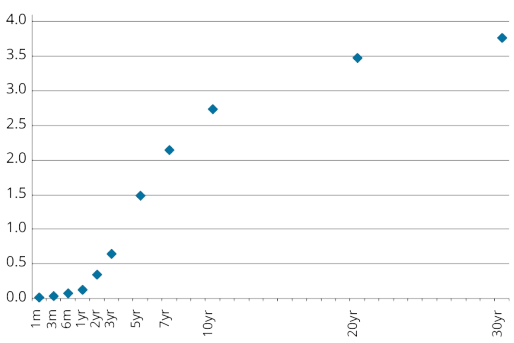

i define and compare the spot curve, yield curve on coupon bonds, par curve, and forward curve;

yield curve: yields by maturity 不同期限债券的收益率

———————————————————-

term structure of interest rates: the yields at different maturities (terms) for like securities or interest rates

spot rate yield curve (spot curve)

aka. zero curve (for zero-coupon) or strip curve (because zero-coupon U.S. Treasury bonds are also called stripped Treasuries)

yield curve for coupon bonds: the YTMs for coupon bonds at various maturities

par bond yield curve** aka par curve: not calculated from yields on actual bonds but is constructed from the spot curve

forward rates: yields for future periods

forward yield curve**: shows the __future rates for the same maturities for __annual periods in the future

Typically, the forward curve would show the yields of 1-year securities for each future year, quoted on a semiannual bond basis

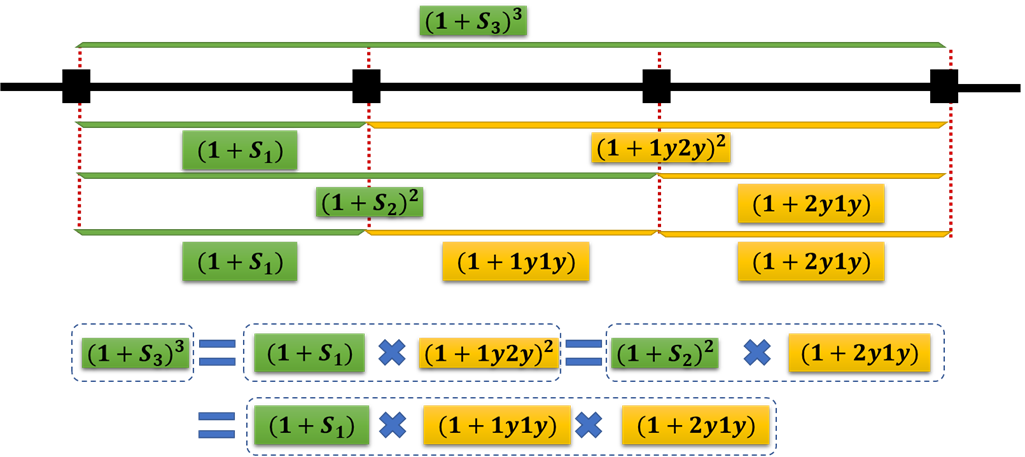

j define forward rates and calculate spot rates from forward rates, forward rates from spot rates, and the price of a bond using forward rates;

notion: 2y**1y is the rate for a 1-year loan to be made **two years from now;

- 利用spot rate计算forward rate

构造两个具有相同现金流的投资组合,其中

A:仅由即期利率资产组成(spot market上的 long-term security)

B: 由即期利率资产(spot market上的short-term security)与远期利率资产

利用二者return相同,计算目标远期汇率

- 无套利方法与简单平均值当法的对比

| 例:The current 1-year spot rate is 4.0%, the current 2-year spot rate is 8.0%, and the current 3-year spot rate is 12.0%. Calculate the 1-year forward rates one and two years from now | | |

| —- | —- | —- |

| info: S1=4.0%, S2=8.0%,S3=12.0% 求:1y1y, 2y1y | | |

| | general form **= | simple averages **≈ |

| |

![[G] Fixed Income - 图18](/uploads/projects/jianzhou@enxqsv/31ee441bc30fea00a5f295e635c1d5a4.svg) |

|

| | 1y1y |

|

| | | 12.154% | 12% | | 2y1y |

|

| | | 20.45% | 20% |

- 利用远期利率进行债券定价

principle: 即期利率与远期利率组合,得到对应时间点的discount rate,然后进行折现、求和

an example ↓

![[G] Fixed Income - 图19](/uploads/projects/jianzhou@enxqsv/6cc355f88afefd300999499390df16b8.svg)

k compare, calculate, and interpret yield spread measures.

yield spread: the difference between the yields of two different bonds

benchmark spread: yield spread relative to a benchmark bond

G-spread: yield spread over a government bond

interpolated spreads aka I**-spreads: Yield spreads relative to swap rates

缺:G-spreads and I-spreads is that they are theoretically correct only if the spot yield curve is flat so that yields are approximately the same across maturities. Normally, however, the spot yield curve is upward-sloping (i.e., longer-term yields are higher than shorter-term yields).

zero volatility spread or Z-spread: 类似于求YTM,归一标准不是‘1’而是‘1+benchmark yield i’

![[G] Fixed Income - 图20](/uploads/projects/jianzhou@enxqsv/54639229bc1e32a791ada376cdbd617c.svg)

option-adjusted spread (OAS)**: the spread to the government spot rate curve that the bond would have if it were option-free

R45 Introduction to Asset-Backed Securities

a explain benefits of securitization for economies and financial markets;

- securitization 证券化

securitization: financial assets are purchased by an entity that then issues securities supported by the cash flows from those financial assets

- primary benefits

- reduction in funding costs for firms selling the financial assets to the securitizing entity

- increase in the liquidity of the underlying financial assets

benefits provided

- 降低中间环节成本→给lender和borrowing让出更多利润空间

- 将mortgage证券化,明确了投资者对抵押资产的声索权

- 提高银行资产的流动性

- 银行可通过资产证券化迅速回收proceed,从而可以产生更多loan

- 适于金融创新,产生风险水平、种类更具个性化的投资选择

- 相比购买私人贷款,资产证券的更具多样性、风险更低

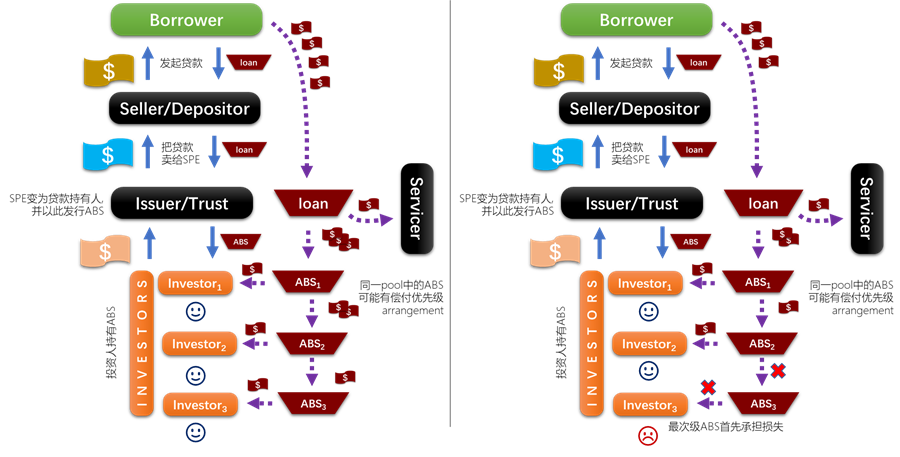

b describe securitization, including the parties involved in the process and the roles they play;

special purpose entity (SPE)

seller/depositor originates the loans and sells the portfolio of loans to SPE

issuer/trust the SPE that buys the loans from the seller and issues ABS to investors

servicer services the loans

mortgage-backed securities (MBS): 转移给SPE的资产为mortgage的ABS

c describe typical structures of securitizations, including credit tranching and time tranching;

tranches: classes in an ABS

waterfall structure: each class of ABS (tranche) is paid sequentially, to the extent possible (tranche or only time tranching?)

credit tranching: first-loss tranche (subordinated) is first to absorb any losses until exceed trach principal, then for the next less subordinated. aka. senior/subordinated structure

- time tranching: the first tranche receives all principal repayments of the tranche. Then for the second tranch

d describe types and characteristics of residential mortgage loans that are typically securitized;

- basic concepts

residential mortgage loan: loan, collateral is residential real estate

loan-to-value ratio, LTV: the percentage of the value of the collateral real estate that is loaned , (lower, better)

![[G] Fixed Income - 图22](/uploads/projects/jianzhou@enxqsv/94aa862bb0d8453caba56e0e4e137e5b.svg)

subprime loans: mortgages to borrowers of lower credit quality, or have a lower-priority claim to the collateral if default

- maturity, interest rate and amortizing

- Maturity: 15~30 yr in U.S.; 20~40 in Europe; …

- Rate

- fixed-rate mortgage

- adjustable-rate mortgage (ARM) aka. variable-rate mortgage

index-referenced mortgage: interest rate根据某一market reference做调整

hybrid mortgage: 固定息(period1)后转换为可调息(period2)

rollover/ renegotiable mortgage: 固定息1(period1)转换到固定息2(period2)

convertible mortgage: 借款人有权将剩余期限内借款从r1(固定/可调)转换为另一种r2**(固定/可调)** 可转期按揭

- Amortization

- fully amortizing

- partially amortizing

- interest-only mortgage

- prepayment

prepayment: partial or full repayment of principal in excess of scheduled principal repayments required by the mortgage

refinances: prepays the remaining principal amount using the proceeds of a new, lower interest rate loan

(低利率时期refinancing可以降低借款人借款成本)

prepayment penalty: an additional payment that must be made if principal is prepaid 为lender提供保护

- foreclosure

丧失抵押品赎回权

nonrecourse loans: 债权人只对collateral property有claim rightl 无追索权贷款

strategic default: 抵押品价格(房价)下跌导致抵押品价值(房屋总价值)小于未偿还本金,borrower选择主动违约

recourse loans: lender has a claim against the borrower for the amount by which the sale of a repossessed collateral property falls short of the principal outstanding on the loan 有权追索出售抵押品所得不及未偿还本金的部分 追索权贷款

e describe types and characteristics of residential mortgage-backed securities, including mortgage pass-through securities and collateralized mortgage obligations, and explain the cash flows and risks for each type;

Residential mortgage-backed securities (RMBS)

- 按发行机构:agency RMBS;nonagency RMBS

- agency RMBS: issued by the Government National Mortgage Association (GNMA or Ginnie Mae, 吉利美), the Federal National Mortgage Association (Fannie Mae,房利美), and the Federal Home Loan Mortgage Corporation (Freddie Mac,房地美)

criteria: minimum percentage down payment最低首期支付, maximum LTV ratio, maximum size, minimum documentation required, insurance purchased by the borrower

conforming loans: meet the criteria; nonconforming loans: do not meet the criteria*

- nonagency RMBS

nonagency RMBS: RMBS NOTissued by GNMA, Fannie Mae, or Freddie Mac

credit enhancement: 信用增级

shifting interest mechanism: If prepayments or credit losses decrease the credit enhancement of the senior securities, the shifting interest mechanism suspends payments to the subordinated securities for a period of time until the credit quality of the senior securities is restored 如果提前还款或者信用受损导致高级tranche的信用增级受损,刺激tranche的利息支付会暂时搁置一段时间,直至高级tranche的信用质量恢复

**

- 按structure:mortgage pass-through securities;collateralized mortgage obligations

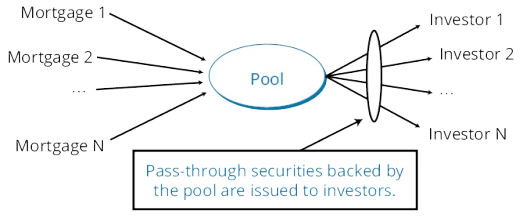

- mortgage pass-through securities: investors_ _receive the monthly cash flows generated by the underlying pool of mortgages, less any servicing and guarantee/insurance fees

securitized mortgage: mortgage included in the pool

weighted average maturity (WAM): weighted average of the final maturities of all the mortgages in the pool

![[G] Fixed Income - 图24](/uploads/projects/jianzhou@enxqsv/18fec499697478fd94ce238a7fdf3c64.svg) (权重为本金额度)

(权重为本金额度)

weighted average coupon (WAC) rate: weighted average of the interest rates of all the mortgages in the pool

pass-through rates: the coupon rate on the MBS aka. net interest or net coupon

The timing of the cash flows to pass-through security holders does not exactly coincide with the cash flows generated by the pool. This is due to the delay between the time the mortgage service provider receives the mortgage payments and the time the cash flows are passed through to the security holders.

- collateralized mortgage obligations (CMO): securities collateralized by RMBS, (securities secured by securities)

Each CMO has multiple bond classes (CMO tranches) that have different exposures to prepayment risk

f define prepayment risk and describe the prepayment risk of mortgage-backed securities;

- prepayment risk

prepayment risk:** 若borrower提前偿还本金,lender将不会再收到这部分本金对应的利息,需要将这部分本金进行再投资

extension risk: prepayments will be slower

contraction risk*: prepayments will be more rapid than expected

_Prepayment rates depend on WAC rate of the loan pool, current interest rates, prior prepayments of principal_

- prepayment risk of MBS & its measure

single monthly mortality rate (SMM): percentage by which prepayments reduce the month-end principal balance, compared to what it would have been with only scheduled principal payments (with no prepayments).

SMM is measured as a per-month percentage of mortgages in the MBS pool that will be paid off early__.

conditional prepayment rate (CPR): annualized measure of prepayments 条件早偿率

Public Securities Association (PSA) prepayment benchmark: assumes that the monthly prepayment rate for a mortgage pool increases as it ages (becomes seasoned)

The PSA benchmark is expressed as a monthly series of CPRs;

CPR (MBS)=CPR(PSA standard benchmark )→PSA = 100 (100% of the benchmark CPR)

- CMO: re-distribute prepayment risk

collateralized mortgage obligations (CMO): securities collateralized by RMBS, (securities secured by securities)

Each CMO has multiple bond classes (CMO tranches) that have different exposures to prepayment risk

CMO资产池中的总提前还款风险不变,但通过不同的tranches进行了再分配。扩大了RMBS的potential market

- primary CMO structures

*sequential-pay tranches, *planned amortization class tranches (PACs), *support tranches, *floating-rate tranches.

- sequential pay CMO separate the cash flows into tranches that are retired sequentially

tranches均接收interest,但本金偿还有特定顺序 from short tranches to other tranches

short traches: extension risk下降,contraction risk上升

other trancher: contraction risk下降,extension risk 上升

- PAC CMO

planned amortization class (PAC): make predictable payments, regardless of actual prepayments to the MBS

PAC tranches的contraction risk和extension __risk均得到降低

support tranches: 吸收 PAC class的 contraction risk 和 extension risk__;还款过快,他先退。还款过慢,他先留

support tranches相对于PAC tranche越大,能为PAC提供的保护就越充分

initial PAC collar: 能使PAC tranche现金流按计划进行的对应的提前还款速率的上限与下限

broken PAC: PAC tranche with payments either sooner or later than promised 失败的PAC

g describe characteristics and risks of commercial mortgage-backed securities;

- basic concept

- commercial mortgage-backed securities CMBS: backed by income-producing real estate 商业抵押担保证券

CMBS mortgages are structured as nonrecourse loans, 故更关注mortgage资产质量

CMBS structure: segregated into tranches, with different priority

- call protection 提前偿还保护

loan-level call protection

Prepayment lockout 特定时期内禁止borrower赎回本金

Defeasance _prepayment不支付给投资人,而用于购买可以满足支付需要的政府债券投资组合

_Prepayment penalty points 根据提前偿还的本金额按比例收取penalty

Yield maintenance charges 除提前偿还的本金,borrower还需支付对应的投资人利息损失

CMBS-level call protection** **

CMBS中分为不同的tranches,风险在其中重新分配

- amortization

Commercial mortgages are typically amortized over a period longer than the loan term

CMBS的securitized mortgage 在maturity会有一个balloon payment,对应产生balloon risk

balloon risk: risk of default because borrower is unable to arrange refinancing to make final balloon payment

在此情况下,lender很有可能会被迫展期,故aka. extension risk

- risk measures

Debt-to-service-coverage ratio (DSC) *higher, better

![[G] Fixed Income - 图25](/uploads/projects/jianzhou@enxqsv/f2380f8027bdcf761676930f5d27d39b.svg)

Net operating income (NOI) is calculated after the deduction for real estate taxes but before any relevant income taxesLoan-to-value ratio *lower, better

h describe types and characteristics of non-mortgage asset-backed securities, including the cash flows and risks of each type;

small business loans, accounts receivable, credit card receivables,

automobile loans, home equity loans, manufactured housing loans

![[G] Fixed Income - 图26](/uploads/projects/jianzhou@enxqsv/1107d68f437cafce43c3f37505464f8b.svg)

| Auto Loan ABS | Credit Card ABS | |

|---|---|---|

| amortization | fully amortizing | nonamortizing |

| prepayment | //prepay if the cars are sold, traded in, or repossessed //prepay if car is stolen or wrecked and the loan is paid off from insurance proceeds //borrower’s voluntary prepayment |

lockout period: 无本金偿还 若在lockout period收到本金,会用其购买新的信用卡应收账款,保持资产池总量相对稳定 |

| other issues | credit enhancement: senior-subordinated structure reserve account *excess interest spread |

early (rapid) amortization; most are floating rate; pay monthly, quarterly, or for longer periods |

i describe collateralized debt obligations, including their cash flows and risks.

- basic concepts

collateralized debt obligation (CDO): issued by an SPE for which the collateral is a pool of debt obligations

collateralized bond obligations (CBO): collateral securities are corporate and emerging market debt

collateralized loan obligations (CLO): supported by a portfolio of leveraged bank loans

Structured finance CDOs: collateral is ABS, RMBS, other CDOs, and CMBS

Synthetic CDOs: collateral is a portfolio of credit default swaps on structured securities

arbitrage CDO: CDOs structured to earn returns from the spread between funding costs and portfolio returns

- cash flow & risks

//Unlike the ABS, CDOs do not rely on interest payments from the collateral pool. CDOs have a collateral **manager who buys and sells **securities in the collateral pool in order to generate the cash to make the promised payments to investors.//

- source of promised payments:

*interest earned on securities, *cash from maturing securities *cash from the sale of securities _

- CDOs issue three classes of bonds (tranches):

|*senior bonds || *mezzanine bonds ||| *subordinated bonds aka. equity or residual tranche

SS15 Fixed Income (2)

R46 Understanding Fixed-Income Risk and Return

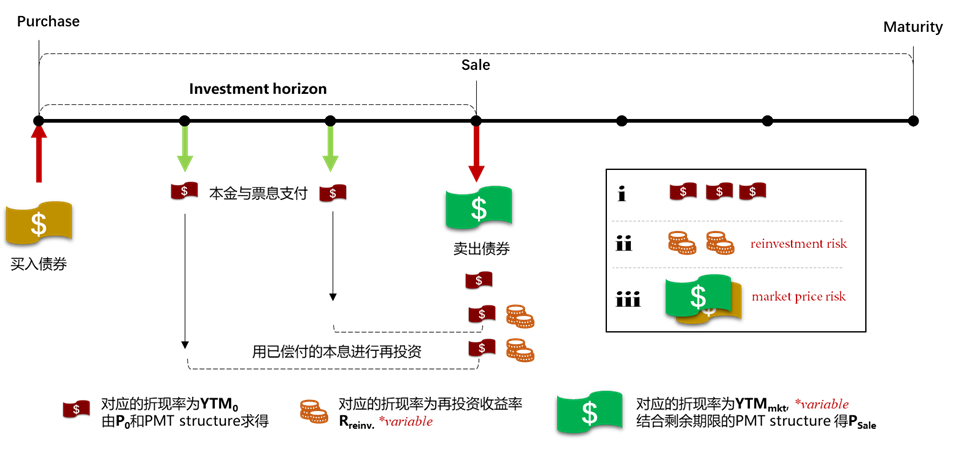

a calculate and interpret the sources of return from investing in a fixed-rate bond;

- sources of return

- i/coupon and principal payments

本息偿还

- ii/interest earned on coupon payments that are reinvested over the investor’s holding period for the bond

在债券期限内用收到的本息进行再投资所获得的收益

- iii/any capitatl gain or loss if the bond is sold prios to maturity

在债券到期前出售债券造成的资本损益

- 简单分析

假设1:no credit risk (ie. 票息支付不存在风险);

假设2:**R=YTM**mkt (rationality:利用收到的票息在即期市场投资债券)

*持有到期,R=YTM**

*到期之前出售,且持有期内YTM**=YTM**恒成立,R=YTM**

*T∈(购买日, 1st 票息日), YTM**⬆⋙ R(buy-and-hold)>YTM0

无资本损益;再投资收益上升

*T∈(购买日, 1st 票息日), YTM**⬆ ⋙ R(short period hold)<YTM0

资本损失;再投资收益上升,但再投资期限较短不足以弥补资本损失

*T∈(购买日, 1st 票息日), YTM**⬇ ⋙R(long period hold )<YTM**0

资本利得,但不足以弥补长期内再投资收益下降带来的损失

market price risk: the uncertainty about price due to uncertainty about _YTM_

reinvestment risk: uncertainty about sum(PMTs and reinv. income on PMTs) due to the uncertainty about future_ reinv. rates**_

| investment horizon | market price risk | reinvestment risk | YTM**⬆** |

|---|---|---|---|

| the uncertainty about price due to uncertainty about__ YTM | uncertainty about sum(PMTs and reinv. income on PMTs) due to uncertainty about__ future__ reinv. rates | ||

| to maturity | None | ❗❗❗ | 🙂 |

| short | ❗❗❗ | ❗ | 🙁 |

| long | ❗ | ❗❗❗ | 🙂 |

**

- 其他概念

annualized holding period rate of return compound annual return earned from the bond over holding period.

investment horizon the time bond will be held

carrying value: the value of a bond at the same YTM0 as when it was purchased, at any T∈investment horizon

b define, calculate, and interpret Macaulay, modified, and effective durations;

duration: sensitivity _of a bond’s _full price to a change in its yield

- Macaulay Duration** **

- definition

Macaulay duration: weighted average _of the number of years_ until each of the bond’s promised cash flows is to be paid 麦考利久期

calculatation

<br />

| C | t | PV | wt | wt×t |

|---|---|---|---|---|

| C1 | 1 | |||

| C2 | 2 | |||

| C3 | 3 | |||

| Macaulay duration | sum(wt×t) |

interpretation

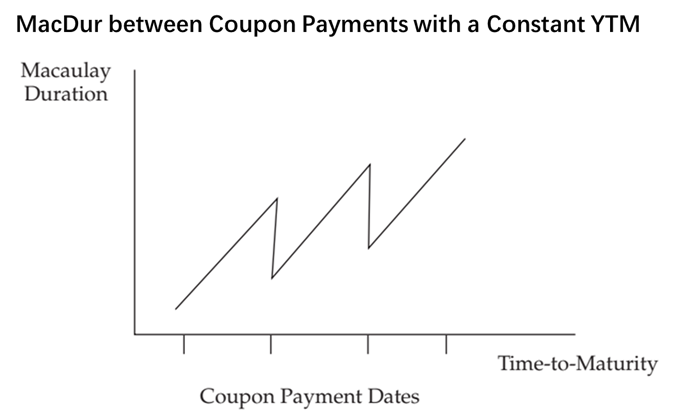

Macaulay duration

weighted-average time to receive principal and interest ,

NOT the best estimate of interest rate sensitivity

*decreases with the passage of time and then goes back up significantly at each PMT date.↓

- Modified Duration

- definition

Modified duration (ModDur): MacDur divided by one plus the bond’s yield to maturity 修正久期

- calculatation

![[G] Fixed Income - 图30](/uploads/projects/jianzhou@enxqsv/37369900338ee1555828b24cdf5b2e4d.svg)

![[G] Fixed Income - 图31](/uploads/projects/jianzhou@enxqsv/3bb324c302ab7dc06a6e875ad4d028c3.svg)

![[G] Fixed Income - 图32](/uploads/projects/jianzhou@enxqsv/247c48d8a9cbbd501833951101d1e774.svg)

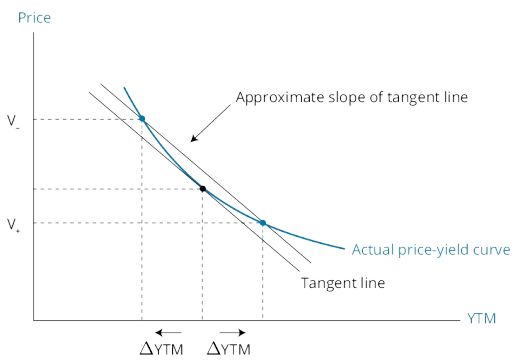

*Approximate Modified Duration: linear approx.good for small change

![[G] Fixed Income - 图33](/uploads/projects/jianzhou@enxqsv/f9811545b307213f9996b0831c48dd02.svg)

- interpretation

当收益率变动1%时,债券价格变动了百分之几

approximate percentage change in bond price = –ModDur × ΔYTM

- Effective Duration

- definition

effective duration: interest rate sensitivity for bonds with embedded options

- calculation

![[G] Fixed Income - 图35](/uploads/projects/jianzhou@enxqsv/7aa6b31f56852d6605578a3d521b3729.svg)

Δcurve, change in the benchmark yield curve used with a bond pricing model

- interpretation

c explain why effective duration is the most appropriate measure of interest rate risk for bonds with embedded options;

effective duration 最适衡量含权债券利率风险

![[G] Fixed Income - 图36](/uploads/projects/jianzhou@enxqsv/4c270437edef4f53d919aa0087a8d7cc.svg)

含权债券现金流影响因素: *future interest rates *the path that interest rates take over time

⬆ **(eg. did they fall to a new level or rise to that level?).

effective duration的计算必须基于针对含权债券的定价模型

含权债券的未来现金流有不确定性,所以基于YTM的计算公式不适用d define key rate duration and describe the use of key rate durations in measuring the sensitivity of bonds to changes in the shape of the benchmark yield curve;

- definition

key rate duration,aka partial duration: sensitivity of bond/portfolio value to changes in the spot rate for a specific __maturity

The basic principle of key rate duration is to change the yield for a particular maturity __of the yield curve and determine the sensitivity of a security or portfolio to that change holding all other yields constant.

- explaination (use)

‘Holding the yield for all other maturities constant, the key rate duration is the approximate percentage change in the value of a portfolio (or bond) for a 100-basis-point change in the yield for the maturity whose rate has been changed.’

there is a vector of durations representing each maturity on the yield curve 会有一组关键利率久期

particularly useful for measuring the effect of a nonparallel shift in the yield curve on a bond portfolio.

*The effect on the overall portfolio is the sum of these individual effects.

e explain how a bond’s maturity, coupon, and yield level affect its interest rate risk;

| 🙂lower interest risk , when | 解释 | |

|---|---|---|

| maturity | maturity decreases | 折现率的幂次⬇,利率对价格的影响⬇ |

| coupon | coupon rate higher | 现金流更多发生在早期,利率对价格的影响⬇ |

| yield level | YTM higher | YTM越大,dP/dYTM越小 |

Adding either a put or a call provision will decrease a straight bond’s interest rate risk as measured by effective duration

f calculate the duration of a portfolio and explain the limitations of portfolio duration;

- calculation

- method 1** **资产组合现金流角度

weighted average number of periods until the portfolio’s cash flows will be received.

theoretically correct but not often used in practice

*not work for a portfolio that contains bonds with embedded options because the future CFs are uncertain

- method 2 组合中资产久期的加权平均

weighted average of the durations of the individual bonds in the portfolio.

typically used in practice

able to calculate duration for a portfolio containing bonds with embedded options by using effective durations.

a practical approximation of the theoretically correct

less accurate when there is greater variation in yields among portfolio bonds,

same as the portfolio duration under the method 1 when the yield curve is flat duration

![[G] Fixed Income - 图38](/uploads/projects/jianzhou@enxqsv/d59d0981062e60e585bb36e1cc906d13.svg)

![[G] Fixed Income - 图39](/uploads/projects/jianzhou@enxqsv/e462c28759a21c17091340dbe0edcdcf.svg)

W**i** = full price of bond i divided by total value of the portfolio; D**i = duration of bond i; N** = number of bonds in the portfolio

- comparision of portfolio duration

| | method 1** 资产组合现金流角度 | method 2 组合中资产久期的加权平均 |

| :—-: | —- | —- |

| advantage | theoretically correct | practical approximation |

| drawback

(limitations)* | 当未来现金流存在不确定性时,无法计算 | ‘parallel shift‘假设须成立

less accurate when greater variation in yields among portfolio bonds |

注:parallel shift: all rates change by the same amount in the same direction

g calculate and interpret the money duration of a bond and price value of a basis point (PVBP);

- money duration**

- calculation

![[G] Fixed Income - 图40](/uploads/projects/jianzhou@enxqsv/fba2825f03dc7ab1da81ad7433c59c86.svg)

![[G] Fixed Income - 图41](/uploads/projects/jianzhou@enxqsv/7ed8f965a2f37d5f816a2330a7d0bd6c.svg)

注意是修正久期乘以价格

- interpretation

现金久期YTM变化=债券价值变化

*![[G] Fixed Income - 图42](/uploads/projects/jianzhou@enxqsv/8c00f95f9012eeeea2517226d40f387b.svg)

- PVBP

price value of a basis point (PVBP): money change in full price of when YTM changes by one basis point (0.01%)

- calculation

计算 V+=V(YTM+0.01); V-=V(YTM-0.01)

计算 PVBP=(V—V+)/2

- interpretation

money change in full price of when YTM changes by one basis point (0.01%)

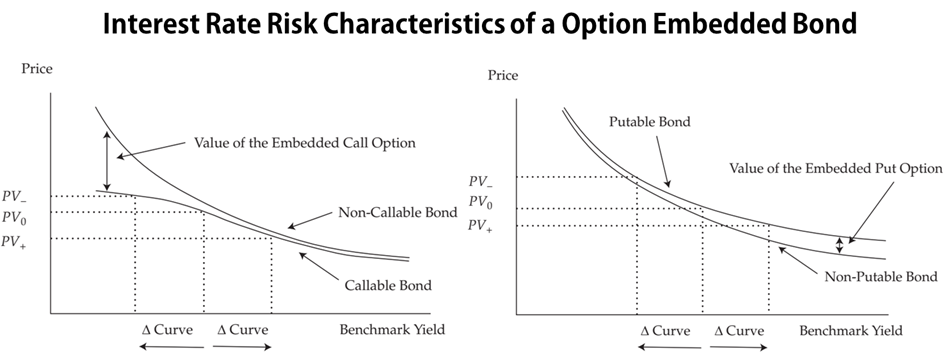

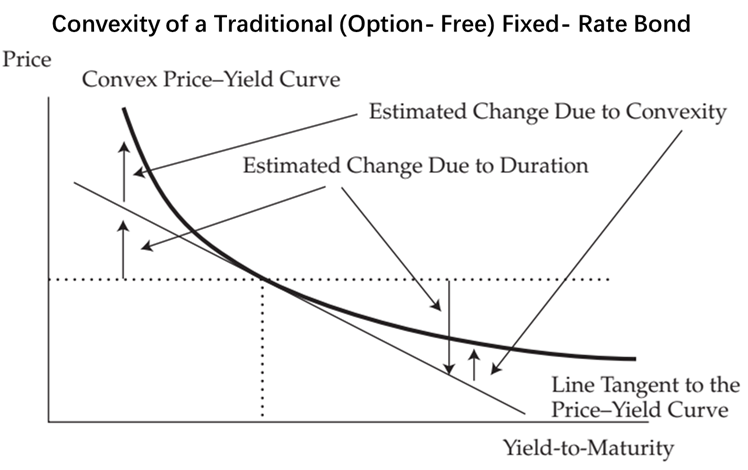

h calculate and interpret approximate convexity and distinguish between approximate and effective convexity;

convexity: measure of the curvature(曲率) of the price-yield relation 凸性.

- apprpximate convexity

calculation

interpretation

The more curved it is, the greater the convexity adjustment to a duration-based estimate of the change in price for a given change in YTM?

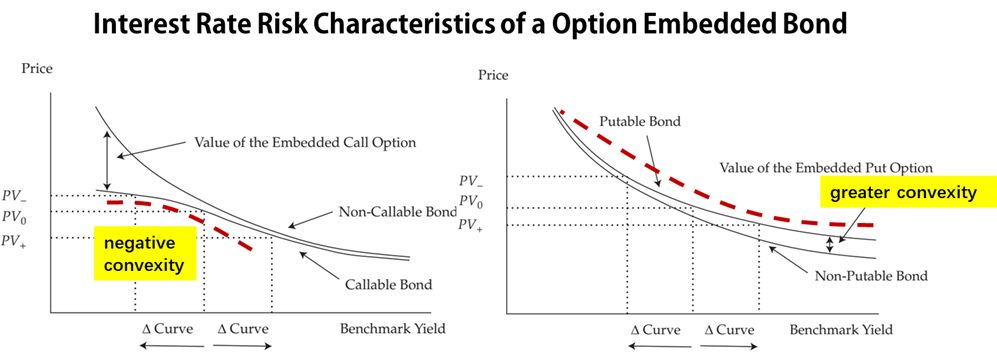

effective convexity

used for bonds with embedded options

![[G] Fixed Income - 图44](/uploads/projects/jianzhou@enxqsv/bae6242c20085879c11c8277bb661870.svg)

a option-free bond (always) has positive convexity,

a callable bond could have negative convexity at low yields

*a putable bond has greater convexity than an otherwise identical option-free bond

i estimate the percentage price change of a bond for a specified change in yield, given the bond’s approximate duration and convexity;

- calculation (an approximation)

![[G] Fixed Income - 图46](/uploads/projects/jianzhou@enxqsv/4b6eb6e176e14bf04495ac7f9aab2972.svg)

j describe how the term structure of yield volatility affects the interest rate risk of a bond;

term structure of yield volatility: relation between volatility of bond yields and their times to maturity

- SOURCE of a bond’s price **volatility**

*债券价格对给定债券**收益率变化的敏感程度 *债券收益率**本身的波动程度

- affects

仅通过久期和凸性计算价格波动时,implicitly assumption: parallel shift

In calculating duration and convexity, we implicitly assumed that yield curve shifted in a parallel manner.

现实中,利率变化往往不是平行移动。(某一因素对不同maturity的yield影响程度不同,即:收益率曲线形状会变化)

例:若短期利率的波动性超过长期利率的波动性,短债价格波动性可能超过长债(即使长期债券的久期更大)

k describe the relationships among a bond’s holding period return, its duration, and the investment horizon;

When investment horizon = Macaulay duration:

a parallel shi**ft in the yield curve _p__rior to the first coupon PMT _will not affect the investor’s horizon return

YTM变化对价格(资本利得)和再投资收益的影响相互抵消( for parallel shift)

duration gap**: difference between a bond’s Macaulay duration and the bondholder’s investment horizon

![[G] Fixed Income - 图48](/uploads/projects/jianzhou@enxqsv/da94a0b50413ee43b5d9da58973f1e53.svg)

| Situation | inv. horizon<MacDur | inv. horizon=MacDur | inv. horizon>MacDur |

|---|---|---|---|

| duration gap | positive | zero | negative |

| greater risk | market price risk | OFFSET | reinvestment risk |

l explain how changes in credit spread and liquidity affect yield-to-maturity of a bond and how duration and convexity can be used to estimate the price effect of the changes.

利差对YTM的影响

![[G] Fixed Income - 图49](/uploads/projects/jianzhou@enxqsv/96ca6306cc5f20d4b747713a6e62e343.svg)

how to estimate

ΔYTM=Δ利差,故计算方式同前(仅考虑利差变化的情况下)<br /> R47 Fundamentals of Credit Analysis

a describe credit risk and credit-related risks affecting corporate bonds;

credit risk: risk of losses because borrower fail to make timely and full payments _of interest or principal

default risk: probability that a borrower (bond issuer) fails to pay interest or repay principal when due

loss severity, aka loss given default: the value a bond investor will lose if the issuer defaults.

expected loss: the default risk multiplied by the loss severity

![[G] Fixed Income - 图50](/uploads/projects/jianzhou@enxqsv/c3b8e9aa5180af25c6a3e45d02ca6dcf.svg)

recovery rate: the percentage of a bond’s value an investor will receive if the issuer defaults

![[G] Fixed Income - 图51](/uploads/projects/jianzhou@enxqsv/b92100e7381f28f51d71b4fb64012bb2.svg)

yield spread 利差 (影响因素:发行人信用等级;债券的流动性)

spread risk: possibility that a bond’s spread will widen

credit migration risk or downgrade risk: possibility that spreads will increase because issuer become less creditworthy

market liquidity risk: risk of receiving less than market value when selling a bond reflected in** bid-ask spreads_.**b describe default probability and loss severity as components of credit risk;

c describe seniority rankings of corporate debt and explain the potential violation of the priority of claims in a bankruptcy proceeding;

- seniority ranking

seniority ranking: bond’s priority of claims to the issuer’s assets and cash flows

secured debt: backed by collateral

first lien or first mortgage (where a specific asset is pledged), senior secured, junior secured debt

unsecured debt/debentures: only represent a general claim to the issue’s assets and cash flows

senior, junior, and subordinated gradations

*pari passu: have same priority of claims

All debt within the same category is said to rank pari passu, or have same priority of claims

- potential violation of the priority

*在债务违约或公司重组时,first ranking理论上具有绝对的优先留置权,但实操时,并不是总严格执行这一原则。公司重组和破产成本较大且耗时较长,过程中需要债权人和股东的投票,为避免由拖延时间造成的额外损失,偿付额度有时通过协商确定,与绝对顺序稍有差别。

d distinguish between corporate issuer credit ratings and issue credit ratings and describe the rating agency practice of “notching”;

- corporate issuer credit rating & issue credit ratings

corporate family ratings (CFR): issuer credit ratings 对债券发行人进行评级

corporate credit ratings (CCR): issue-specific ratings 对债券进行评级

| 投资级 | Moody’s | Aaa | Aa1 | Aa2 | Aa3 | A1 | A2 | A3 | Baa1 | Baa2 | Baa3 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Standard & Poor’s, Fitch | AAA | AA+ | AA | AA- | A+ | A | A- | BBB+ | BBB | BBB- | |||

| 非投资级 | Moody’s | Ba1 | Ba2 | Ba3 | B1 | B2 | B3 | Caa1 | Caa2 | Caa3 | Ca | C | C |

| Standard & Poor’s, Fitch | BB+ | BB | BB- | B+ | B | B- | CCC+ | CCC | CCC- | CC | C | D |

investment grade 投资级

noninvestment grade 非投资级,high yield bonds/junk bonds

cross default provision: When a company defaults on one of its several outstanding bonds, provisions in bond indentures may trigger default on the remaining issues as well 交叉违约

- notching

notching: assignment of individual issue ratings that are higher or lower than that of the issuer

For firms with high overall credit ratings, differences in expected recovery rates among a firm’s individual bonds are less important, so their bonds might not be notched at all. 信用好的公司违约概率较低,没必要notching

For firms with higher probabilities of default (lower ratings), differences in expected recovery rates among a firm’s bonds are more significant. 信用差的公司违约概率较高,违约时偿付顺序较重要,有必要notching

structural subordination: 子公司的债务合同要求在还本付息之前不得将现金tranfer至母公司,在这种情况下,母公司的债务的实际偿还优先级要低于子公司的债务,即使没有明确的tranches structure安排(结构性次级)

e explain risks in relying on ratings from credit rating agencies;

- Credit ratings are dynamic 信用评级动态调整(高信用公司较低信用公司稳定)

- Rating agencies are not perfect 会出现错误评级的状况(例:次贷危机前的次级贷款评级)

- Event risk is difficult to assess 单个公司/行业面临的风险难以合理纳入评级(例:烟草行业的法律风险;自然灾害)

Credit ratings lag market pricing 评级较利率/利差等更新频率较低,且只反映违约风险

f explain the four Cs (Capacity, Collateral, Covenants, and Character) of traditional credit analysis;

four Cs of credit analysis: capacity, collateral, covenants, and character.

- C**apacity** 公司按时还本付息的能力

- Industry structure: Porter’s five forces

- Industry fundamentals: *Industry cyclicality *Industry growth prospects *Industry published statistics

- Company fundamentals: Competitive position Operating history *Management’s strategy and execution

- C**apacity** 公司按时还本付息的能力

*Ratios and ratio analysis

- C**ollateral**

- Intangible assets

Patents🙂, high-quality,more easily sold to generate cash flows than other intangibles.

Goodwill🙁, not a high-quality intangible asset, usually written down during poor performance

- _**Depreciation**_

High (depreciation expense/ capital expenditures) may signal management is not investing sufficiently

The quality of the company’s assets may be poor, may lead to reduced CFO and potentially high loss severity.

- _**Equity market capitalization**_

A stock that trades below book value may indicate that company assets are of low quality.

- _**Human and intellectual capital**** **_

A company may have intellectual property that can function as collateral

- C**ovenants**

- Affirmative covenants** **

paying interest, principal, and taxes; carrying insurance on pledged assets;

continuing in its current business activity; *following relevant laws and regulations

- _**Negative covenants**_

限制股利支付与股票回购; 限制发行新债; 限制发行更优先级债券; 限制兼并收购

对使用未抵押资产作为抵押发行新债的限制; 限制资产出售; 限制公司投资范围;

- C**haracter**

management’s integrity and its commitment to repay the loan

- _**Soundness of strategy**** **_

- _**Track record**_

- _**Accounting policies and tax strategies**_

- _**Fraud and malfeasance record**_

- _**Prior treatment of bondholders**** **_

g calculate and interpret financial ratios used in credit analysis;

- Profits and Cash Flows

EBITDA: Earnings before interest, taxes, depreciation, and amortization

FFO: Funds from operations

net income from continuing operations__ plus depreciation, amortization, deferred taxes, and noncash items__.

Free cash flow before dividends:

net income plus+ depreciation and amortization minus- capital expenditures minus- increase in working capital

Free cash flow after dividends: free cash flow before dividends minus the dividend

- RATIOS

| | Ratios | 🙂

(lower credit risk) | Note | | —- | —- | :—-: | —- | | Leverage Ratios | Debt/capital | lower | Capital=total debt+equity

可根据无形资产进行调整 | | | Debt/EBITDA | lower | more volatile for firms in cyclical industries or with high operating leverage | | | FFO/debt | higher | | | | FCF after dividends/debt | higher | | | Coverage Ratios | EBITDA/interest expense | higher | used more often & also higher than

EBIT-to-interest expense ratio | | | EBIT/interest expense | higher | more conservative(去除了折旧和摊销) |

h evaluate the credit quality of a corporate bond issuer and a bond of that issuer, given key financial ratios of the issuer and the industry;

i describe factors that influence the level and volatility of yield spreads;

不含权债券的收益率构成

yield on an option-free corporate bond=**real risk-free interest ratea

+expected inflation ratea

+maturity premiuma

+liquidity premiumb**

+**credit spread**b

|a__: all bond prices and yields are affected by changes in the first three

|b: last two are the yield spread__

yield spread = liquidity premium + credit spread**

Yield spreads** on corporate bonds are affected primarily by five interrelated factors:

| FACTOR | 🙂Yield spreads narrows when | 🙁Yield spreads widens when |

|---|---|---|

| Credit cycle | the credit cycle improves | the credit cycle deteriorates |

| Economic conditions | economy strengthens | economy weakens |

| Financial market performance | strong-performing markets investors reach for yield in low volatility market |

weak-performing markets |

| Broker-dealer capital | broker-dealers provide sufficient capital | market-making capital becomes scarce |

| General market demand and supply | high demand for bonds | low demand for bonds; excess supply conditions |

*Yield spreads on lower-quality issues tend to be more volatile than spreads on higher-quality issues.

j explain special considerations when evaluating the credit of high yield, sovereign, and non-sovereign government debt issuers and issues.

- High Yield Debt** **

- high yield bonds≈hybrid of investment grade bonds and equity.

Compared to investment grade, high yield bonds show greater price & spread volatility and are more highly correlated with equity market.

- reasons for low rating

High leverage. Unproven operating history. Low or negative free cash flow.

High sensitivity to business cycles. Low confidence in management. Unclear competitive advantages.

Large off-balance-sheet liabilities. Industry in decline

- Special considerations

- liquidity

six sources of liquidity, reliability

B/S cash term>Working capital>Operating cash flow (CFO)>Bank credit>Equity issued>Sales of assets

- financial projections

Projecting future earnings and cash flows, including stress scenarios and accounting for changes in capital expenditures and working capital

important for revealing potential vulnerabilities to the inability to meet debt payments.

- debt structure

公司一般发行不同等级的垃圾债,故每个垃圾债对应的loss severity会有不同

secured bank debt, second lien debt, senior unsecured debt, subordinated debt, and *preferred stock.

(Some of these, especially subordinated debt, may be convertible to common shares.)

top heavy: (垃圾债券)发行人的 secured bank debt占比较大; 其unsecured debt违约概率更高且recovery rates 更低

- corporate structure

holding company structure类型的发行人存在’structural subordination’问题,导致控股公司债的实际的偿付优先级很靠后,子公司上交的股利可能不足支撑timely payment

尽管存在structural subordination, 母公司的评级仍可能较子公司高,因为其有更多融资途径

Some complex corporate structures have intermediate holding companies that carry their own debt and do not own 100% of their subsidiaries’ stock. These companies are typically a result of mergers, acquisitions, or leveraged buyouts

Default of one subsidiary may not necessarily result in cross default.

需结合 bonds’ indentures and other legal documents 判断违约透过公司结构对各个层级的影响.

- covenants

Change of control put lender有权利要求borrower在有收购行为时,按照协议价格(par or slight higher)赎回债务

Restricted payments 限制流向equity holder的现金流

Limitations on liens 限制发行人有担保债务的总量

Restricted versus unrestricted subsidiaries 通过 restriced subsidiary条款避免structural subordination

/对于投资级公司,一般仅在收购行为导致公司信用评级下降时有put option/

银行的债务条款通常更为严格 *在violation更正前 block additional loans ;

*trigger a default by accelerating the full repayment for a unremedied violation

- Sovereign Debt** **

Factors: gov.’s *ability to service debt and its *willingness to do so

The assessment of willingness is important, as bondholders usually have no legal recourse if a national gov. refuses to pay its debts

| BASIC ANALYSIS FRAMEWOORK | |

|---|---|

| Institutional assessment | *successful policymaking; *minimal corruption; *checks and balances among institutions; *culture of honoring debts |

| Economic assessment | *growth trends, *income per capita *diversity of sources for economic growth. |

| External assessment | *foreign reserves, *external debt, *status of its currency in international markets |

| Fiscal assessment | *willingness and ability to increase revenue or cut expenditures to ensure debt service *trends in debt as a percentage of GDP |

| Monetary assessment | *ability to use monetary policy for domestic economic objectives *credibility and effectiveness of monetary policy |

- 两类rating:*local currency debt rating | *foreign currency debt rating

- Sovereign defaults can be caused by events such as war, political instability, severe devaluation of the currency, or large declines in the prices of the country’s export commodities

- Non-Sovereign Government Bonds** **

Non-sovereign government debt; Municipal bonds

- 两类市政债券

General obligation (GO) bonds: unsecured bonds backed by the full faith credit of the issuing governmental entity

Revenue bonds: issued to finance specific projects, such as airports, toll bridges, hospitals

- issues

市政公债不能通过货币政策来满足债务需求,必须通过平衡预算产生足够的现金流

地方政府的偿债能力最终取决于地方经济(tax base)

经济因素:就业, 人均收入/债务则增长, tax base dimensions (depth, breadth, stability), 人口, , 就业吸引力 (location, 基建).

资本利得税、销售税收入等受经济周期影响会有较大波动,需关注地方政府对此类税收的依赖程度

*地方政府的养老金、退休金obligations可能会有较大资金需求

不同政府发行人提供的financial info内容可能不同 ‘Inconsistent reporting requirements’

revenue bonds 的风险更高,因为其现金流仅产生于相应的项目

若有收获,就点个赞吧

0 人点赞