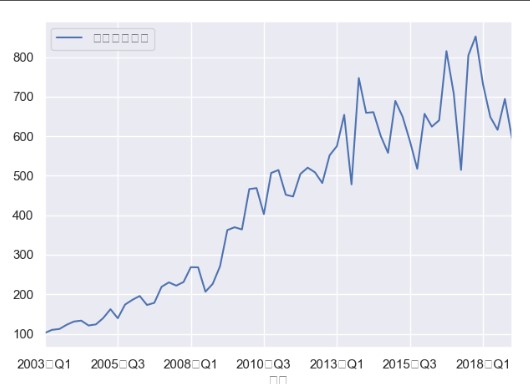

题目:03年到19年第一季度分季度的数据,13年之前只有传统汽车的销量,13年之后是传统汽车+新能源汽车的销量,需要预测未来三期传统汽车的销量~

import pandas as pdimport matplotlib.pyplot as pltdata = pd.read_excel("C:\orange_credit\crdt\时序数据.xlsx", sheet_name='Sheet2', index_col=u'日期')#先画出日期和传统车型销量的图形,可以判断是非平稳的data.plot()plt.show()

所使用的源代码:

def test_stationarity(timeseries):# 滚动平均rolmean = pd.rolling_mean(timeseries, window=12)rolstd = pd.rolling_std(timeseries, window=12)ts_diff = timeseries - timeseries.shift()orig = timeseries.plot(color='blue', label='Original')mean = rolmean.plot(color='red', label='Rolling Mean')std = rolstd.plot(color='black', label='Rolling Std')diff = ts_diff.plot(color='green', label='Diff 1')plt.legend(loc='best')plt.title('Rolling Mean & Standard Deviation')plt.show(block=False)# adf检验print('Result of Dickry-Fuller test')dftest = adfuller(timeseries, autolag='AIC')dfoutput = pd.Series(dftest[0:4], index=['Test Statistic', 'p-value', '#Lags Used', 'Number of observations Used'])for key, value in dftest[4].items():dfoutput['Critical value(%s)' % key] = valueprint(dfoutput)#test_stationarity(ts)def test_stationarity(timeseries):# 滚动平均#差分#标准差rolmean = pd.rolling_mean(timeseries, window=12)ts_diff = timeseries - timeseries.shift()rolstd = pd.rolling_std(timeseries, window=12)orig = timeseries.plot(color='blue', label='Original')mean = rolmean.plot(color='red', label='Rolling 12 Mean')std = rolstd.plot(color='black', label='Rolling 12 Std')diff = ts_diff.plot(color='green', label='Diff 1')plt.legend(loc='best')plt.title('Rolling Mean and Standard Deviation and Diff 1')l1 = plt.axhline(y=0, linewidth=1, color='yellow')plt.show(block=False)# adf--AIC检验print('Result of Augment Dickry-Fuller test--AIC')dftest = adfuller(timeseries, autolag='AIC')dfoutput = pd.Series(dftest[0:4], index=['Test Statistic', 'p-value', 'Lags Used','Number of observations Used'])for key, value in dftest[4].items():dfoutput['Critical value(%s)' % key] = valueprint(dfoutput)# adf--BIC检验print('-------------------------------------------')print('Result of Augment Dickry-Fuller test--BIC')dftest = adfuller(timeseries, autolag='BIC')dfoutput = pd.Series(dftest[0:4], index=['Test Statistic', 'p-value', 'Lags Used','Number of observations Used'])for key, value in dftest[4].items():dfoutput['Critical value(%s)' % key] = valueprint(dfoutput)test_stationarity(ts)# 不取对数,直接减掉趋势ts.index = ts.index.to_timestamp()moving_avg = pd.rolling_mean(ts, 12)plt.plot(ts)plt.plot(moving_avg, color='red')plt.show()ts_moving_avg_diff = ts - moving_avgts_moving_avg_diff.head(12)# 再一次确定平稳性ts_moving_avg_diff.dropna(inplace=True)test_stationarity(ts_moving_avg_diff)expwighted_avg = pd.ewma(ts, halflife=12)plt.plot(ts)plt.plot(expwighted_avg, color='red')plt.show()# 减掉指数平滑法ts_ewma_diff = ts - expwighted_avgtest_stationarity(ts_ewma_diff)# 差分法1ts_diff = ts - ts.shift()plt.plot(ts_diff)plt.show()# 差分方法2fig = plt.figure(figsize=(12, 8))ax1 = fig.add_subplot(111)diff1 = ts.diff(1)# diff2 = diff1.diff(1)diff1.plot(ax=ax1)plt.show()ts_diff.dropna(inplace=True)test_stationarity(ts_diff)plt.show()from statsmodels.tsa.seasonal import seasonal_decomposedecomposition = seasonal_decompose(ts)trend = decomposition.trendseasonal = decomposition.seasonalresidual = decomposition.residplt.subplot(411)plt.plot(ts, label='Original')plt.legend(loc='best')plt.subplot(412)plt.plot(trend, label='Trend')plt.legend(loc='best')plt.subplot(413)plt.plot(seasonal, label='Seasonality')plt.legend(loc='best')plt.subplot(414)plt.plot(residual, label='Residuals')plt.legend(loc='best')plt.tight_layout()plt.show()# 直接对残差进行分析,我们检查残差的稳定性ts_decompose = residualts_decompose.dropna(inplace=True)test_stationarity(ts_decompose)fig = plt.figure(figsize=(12, 8))ax1 = fig.add_subplot(211)fig = sm.graphics.tsa.plot_acf(ts_diff, lags=20, ax=ax1)ax1.xaxis.set_ticks_position('bottom')fig.tight_layout();ax2 = fig.add_subplot(212)fig = sm.graphics.tsa.plot_pacf(ts_diff, lags=20, ax=ax2)ax2.xaxis.set_ticks_position('bottom')plt.show()fig.tight_layout();# trendfig = plt.figure(figsize=(12, 8))ax1 = fig.add_subplot(211)fig = sm.graphics.tsa.plot_acf(trend, lags=20, ax=ax1)ax1.xaxis.set_ticks_position('bottom')fig.tight_layout();ax2 = fig.add_subplot(212)fig = sm.graphics.tsa.plot_pacf(trend, lags=20, ax=ax2)ax2.xaxis.set_ticks_position('bottom')plt.show()fig.tight_layout();# seasonalfig = plt.figure(figsize=(12, 8))ax1 = fig.add_subplot(211)fig = sm.graphics.tsa.plot_acf(seasonal, lags=20, ax=ax1)ax1.xaxis.set_ticks_position('bottom')fig.tight_layout();ax2 = fig.add_subplot(212)fig = sm.graphics.tsa.plot_pacf(seasonal, lags=20, ax=ax2)ax2.xaxis.set_ticks_position('bottom')plt.show()fig.tight_layout();import itertools# Define the p, d and q parameters to take any value between 0 and 2p = d = q = range(0, 3)# Generate all different combinations of p, q and q tripletspdq = list(itertools.product(p, d, q))print('p,d,q', pdq, '\n')for param in pdq:try:model = ARIMA(ts_diff, order=param)# model=ARIMA(ts_log,order=(2,1,2))result_ARIMA = model.fit(disp=-1)print('ARIMA{}-- AIC:{} -- BIC:{} --HQIC:{}'.format(param, result_ARIMA.aic, result_ARIMA.bic, result_ARIMA.hqic))except:continue# AR modelmodel = ARIMA(seasonal, order=(2, 0, 0))result_AR = model.fit(disp=-1)plt.plot(seasonal)plt.plot(result_AR.fittedvalues, color='blue')plt.title('RSS:%.4f' % sum(result_AR.fittedvalues - seasonal) ** 2)plt.show()# AR modelmodel = ARIMA(ts_diff, order=(2, 0, 0))result_AR = model.fit(disp=-1)plt.plot(ts_diff)plt.plot(result_AR.fittedvalues, color='blue')plt.title('RSS:%.4f' % sum(result_AR.fittedvalues - ts_diff) ** 2)plt.show()# MA modelmodel = ARIMA(ts_diff, order=(0, 0, 2))result_MA = model.fit(disp=-1)plt.plot(ts_diff)plt.plot(result_MA.fittedvalues, color='blue')plt.title('RSS:%.4f' % sum(result_MA.fittedvalues - ts_diff) ** 2)plt.show()# ARIMA 将两个结合起来 效果更好# warnings.filterwarnings("ignore") # specify to ignore warning messagesimport itertools# Define the p, d and q parameters to take any value between 0 and 2p = d = q = range(0, 3)# Generate all different combinations of p, q and q tripletspdq = list(itertools.product(p, d, q))print('p,d,q', pdq, '\n')for param in pdq:try:model = ARIMA(ts_diff, order=param)# model=ARIMA(ts_log,order=(2,1,2))result_ARIMA = model.fit(disp=-1)print('ARIMA{}- AIC:{} - BIC:{} - HQIC:{}'.format(param, result_ARIMA.aic, result_ARIMA.bic, result_ARIMA.hqic))except:continue# MA# model=ARIMA(ts_log,order=(2,1,2))model = ARIMA(ts_diff, order=(0, 0, 2))result_ARIMA_diff = model.fit(disp=-1)plt.plot(ts_diff)plt.plot(result_ARIMA_diff.fittedvalues, color='blue')plt.title('RSS:%.4f' % sum(result_ARIMA_diff.fittedvalues - ts_diff) ** 2)plt.show()# ARMA# model=ARIMA(ts_log,order=(2,1,2))model = ARIMA(ts_diff, order=(1, 0, 2))result_ARIMA_diff = model.fit(disp=-1)plt.plot(ts_diff)plt.plot(result_ARIMA_diff.fittedvalues, color='blue')plt.title('RSS:%.4f' % sum(result_ARIMA_diff.fittedvalues - ts_diff) ** 2)plt.show()# 检验部分fig = plt.figure(figsize=(12, 8))ax1 = fig.add_subplot(211)fig = sm.graphics.tsa.plot_acf(result_ARIMA_diff.resid.values.squeeze(), lags=40, ax=ax1)ax2 = fig.add_subplot(212)fig = sm.graphics.tsa.plot_pacf(result_ARIMA_diff.resid, lags=40, ax=ax2)plt.show()import statsmodels.api as smprint(sm.stats.durbin_watson(result_ARIMA_diff.resid.values))# 2附近即不存在一阶自相关# 检验结果是2.02424743723,说明不存在自相关性。resid = result_ARIMA_diff.resid # 残差fig = plt.figure(figsize=(12, 8))ax = fig.add_subplot(111)fig = qqplot(resid, line='q', ax=ax, fit=True)plt.show()# LJ检验r, q, p = sm.tsa.acf(result_ARIMA_diff.resid.values.squeeze(), qstat=True)data = np.c_[range(1, 41), r[1:], q, p]table = pd.DataFrame(data, columns=['lag', "AC", "Q", "Prob(>Q)"])print(table.set_index('lag'))# model=ARIMA(ts_log,order=(2,1,2))model_results = ARIMA(ts_diff, order=(1, 0, 2))result_ARIMA = model_results.fit(disp=-1)# fig, ax = plt.subplots(figsize=(12, 8))# ax = ts.ix['1962':].plot(ax=ax)# fig = result_ARIMA.plot_predict('1976-01', '1976-12', dynamic=True, ax=ax, plot_insample=False)result_ARIMA.plot_predict()result_ARIMA.forecast()plt.show()predictions_ARIMA_diff = pd.Series(result_ARIMA_diff.fittedvalues, copy=True)print(predictions_ARIMA_diff.head())print('------------------------')predictions_ARIMA_diff_cumsum = predictions_ARIMA_diff.cumsum()print(predictions_ARIMA_diff_cumsum.head())predictions_ARIMA = pd.Series(ts.ix[0], index=ts.index)predictions_ARIMA_cus = predictions_ARIMA.add(predictions_ARIMA_diff_cumsum, fill_value=0)predictions_ARIMA_cus.head()plt.plot(ts)plt.plot(predictions_ARIMA_cus)plt.title('RMSE: %.4f' % np.sqrt(sum((predictions_ARIMA_cus - ts) ** 2) / len(ts)))plt.show()# 对的--加上了预测的值predict_dta = result_ARIMA_diff.predict('1976-01', '1976-12', dynamic=True)AA = predictions_ARIMA_diff.append(predict_dta)predictions_ARIMA = pd.Series(ts.ix[0], index=pd.period_range('196202', '197612', freq='M'))AA.index = pd.period_range('196202', '197612', freq='M')predictions_ARIMA2 = predictions_ARIMA.add(AA.cumsum(), fill_value=0)ts.plot()predictions_ARIMA2.plot()plt.show()

若有收获,就点个赞吧

0 人点赞